172,000 job opportunities. A negative real wage week can shake things up.

Listen to the audio version of this article (generated by artificial intelligence).

The jobs report that Main Street wanted, Wall Street didn’t… Consumer headline… Artificial intelligence displacement gets new data… A week that could move everything

As I write on Monday morning, markets are trying to recover from last Friday’s technical debacle sparked by a massive jobs report – which was the last thing an inflation-shattered market wanted to see.

The May employment report came in well above expectations. The United States added a seasonally adjusted 172,000 jobs in May, more than double expectations of 80,000 jobs. Meanwhile, the unemployment rate stabilized at 4.3%.

Looking back, payroll gains averaged 188,000 over the past three months — a pace not seen since March 2024.

Now, this sounds like great news – so why Friday’s tech meltdown?

Because the report came on top of the latest Personal Consumption Expenditure (PCE) inflation reading of 3.8% – the highest since May 2023 – and two consecutive episodes of inflation trending in the wrong direction. A strong labor market, in this environment, gives the Fed no room to cut interest rates. If anything happens, the conversation will now move to the rate Hiking.

White House National Economic Council Director Kevin Hassett said Bloomberg The TV said investors were “deeply wrong” to interpret the strong report as evidence that the Fed will raise interest rates — his argument: Oil price shocks historically lead to temporary, not permanent, inflation.

We’ll find out soon enough. Fed officials meet next week under new Chairman Kevin Warsh — and Friday morning’s data made that meeting considerably more interesting.

But Fed policy aside, is this report really a glowing reflection of the health of Main Street?

Let’s break it down.

Title versus what’s underneath

Friday’s jobs numbers look strong on the surface. Below is a different picture.

In addition to the 172,000 new jobs, the same report showed that year-over-year average hourly wages rose just 3.4% in May – down from 3.6% in April. With PCE inflation at 3.8%, this means that real wages are very negative. Translation: Workers get raises that don’t keep up with what they pay at the pump and the grocery store.

On the other hand, the long-term unemployment rate – people out of work for 27 weeks or more – jumped to 27.5% in May. This is up from 25.3% in April, the highest level since December 2021.

So, beneath the shiny headline of “172,000 jobs,” there are ever-widening cracks.

It gets more complicated…

Even as long-term unemployment rates rise and real wages fall, says our technology expert Luke Lango, magazine editor Innovation investorA strange paradox may follow.

Here’s Luke:

Nominal personal spending growth rose in April from 5.7% to 5.9%, the strongest reading since January 2025.

Consumers did not withdraw at all. If anything, they spend more. But the basic support for this spending completely collapsed underneath them.

So, if wages don’t fund this huge spending, what does?

Savings.

Locke notes that the personal savings rate in the United States collapsed to 2.6% in April 2026 – one of its lowest levels in modern history.

But savings are not the only source of this spending, it also comes from debt. Some cracks form.

here CBS News:

Credit card delinquency rates across the United States have reached their highest levels since 2011…

Nationally, about 13% of all credit card accounts were delinquent in the first quarter.

CBS He went on to report data from Fidelity that more Americans are taking out loans and making hard withdrawals from their 401(k) retirement accounts.

So while Friday’s headline unemployment rate suggests the labor market is getting stronger, the picture for the US consumer is considerably more worrying.

here Wall Street JournalSummary of what happened on Friday:

American consumers reported feeling miserable about the economy, gasoline prices, inflation and the job market.

A key measure of consumer confidence has hit all-time lows in recent months amid concern about future inflation.

Where is all this taking us?

Here are Luke’s latest predictions:

Over the next 12 months, the consumer situation is going from bad to worse.

Sometime in 2027, they hit a wall. Spending collapses. Drill consumer confidence.

Since consumer spending still makes up about 70% of US GDP, the broader economy is beginning to collapse.

And here begins the story of the AI job displacement we have been tracking.

Locke predicts that when the economy begins to collapse, corporate revenues will suffer. So how will the administration respond?

By accelerating the shift from human workers to artificial intelligence.

This dynamic feeds directly into Locke’s predictions about the “2028 election” – where a bipartisan populist anti-AI movement pushes legislation. This may look like different things – perhaps a tax on AI profits, or a forced limit on large-scale capital expenditures, or perhaps mandatory audits of new AI models – but whatever the form, it derails AI business.

Back to Luke:

By late 2028 or early 2029, these politicians will continue…

This is the March 2000 moment for the AI bull market.

We will continue to track this.

And on that note, last Thursday, the data gave us something new to track…

The AI jobs discussion got more data

Over the past few months, I’ve been in what I call a “convince me” position about job displacement due to AI.

A long time ago digest Readers know I’ve spent years reporting on risks. But over the past 12 months, I have encountered increasing data and analysis that contradicts this narrative. At least in his timing.

Recently, I came across research by Citadel Securities indicating that job postings in sectors exposed to AI are now… to risedoes not fall. Meanwhile, executives are framing AI as a complement to their workforce, not a replacement for it.

Today, although I still worry about the job displacement theory, I hold to it with less conviction than before as I track the data, which brings us to last Thursday’s Challenger, Gray and Christmas report.

the address:

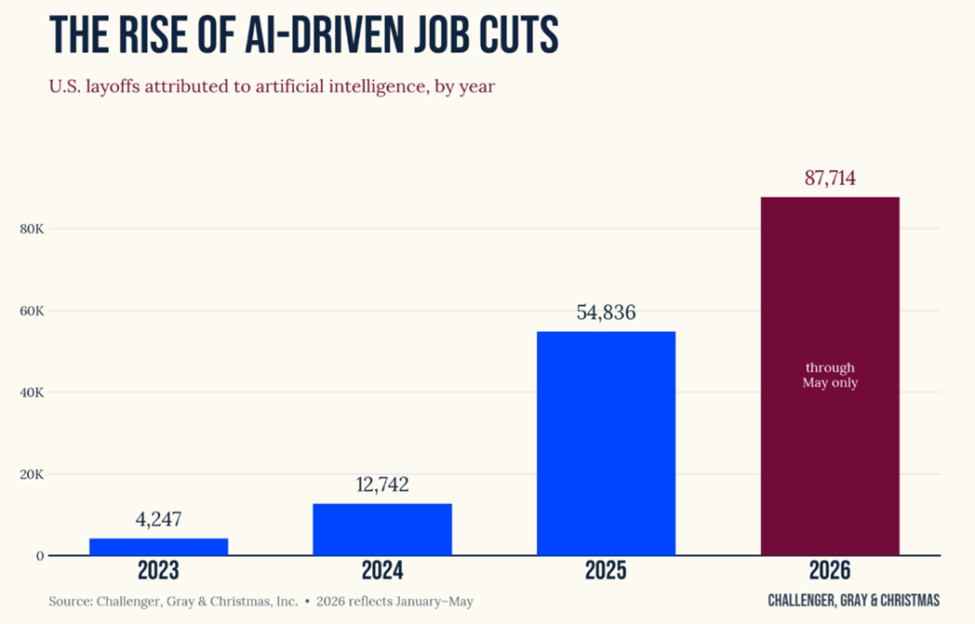

AI brings May sales to 97,006, the highest May total since 2020.

For the third month in a row, companies cited artificial intelligence as the main reason for layoffs – accounting for 40% of all cuts in May.

Job cuts due to AI have now reached 87,714 jobs so far this year, an increase of almost 60% compared to all of 2025, with seven months to go.

Luke saw the report and gave a clear answer:

Jevons’ paradox… Learn about Engels’ pause.

To make sure we’re all on the same page, Jevons’s paradox holds that as a resource becomes more efficient, the overall consumption of that resource tends to rise rather than fall.

Applicable to AI: AI may be cheaper and more capable Expand demand on the workers who employ it, not reduce it.

On the other hand, the “Engels Pause” refers to a period during the Industrial Revolution in Britain – roughly 1790 to 1840 – when GDP growth exploded, corporate profits rose, while average real wages for workers remained constant or declined for fifty years.

The wealth eventually flowed in. The jobs eventually doubled. But it took half a century.

AI compresses the same dynamic into a single decade, Locke says. It took a century for the steam engine to be popularized. ChatGPT reached 100 million users in 2 months.

So, while Jevons’s argument has believers, Luke is not one of them—at least not now:

Although I understand these arguments in the long term, I’m not sure I buy them in the short term, because the numbers and ads tell a fairly clear story.

That story added a new chapter last Thursday.

We will continue to follow this development here at digest.

What’s driving volatility this week?

If Friday’s 4.2% decline in the Nasdaq has you feeling uneasy, you’re not out of the woods yet. This week is full of catalysts that could move the markets.

Wednesday comes the May CPI report – the latest data on the impact of the Iran war on consumer costs.

Thursday is followed by the Producer Price Index, which shows how the same inflation affects businesses.

Friday brings the latest consumer confidence report.

All of this feeds directly into the Fed’s calculations ahead of next week’s Federal Open Market Committee meeting, now the Fed’s most important meeting in years.

New Chairman Warsh will have to weigh Friday’s strong labor market reading against inflation at nearly double the Fed’s target — with rate hike pressure mounting from multiple directions.

Now, amidst this crowded calendar, there’s another wildcard.

On Friday, SpaceX is expected to price its IPO at $75 billion, which is already oversubscribed, according to Bloomberg. This could be the largest IPO in history, arriving in the middle of one of the most important macro weeks in recent memory.

Luke has prepared his subscribers for this moment — and his take might surprise you. Buying a historic IPO on day one is usually the wrong trade.

Here’s Luke:

The biggest gains from tech IPOs never go to investors who bought on day one. They went to investors who owned the ecosystem around those companies before Wall Street came along to reprice it.

This is exactly the opportunity I’ve been preparing for. I call it Back door before IPO – A small group of publicly traded companies that power and leverage both OpenAI and Anthropic, and I believe will be repriced significantly the moment their S-1 filings arrive.

The entry window before the requote is now open. I don’t know how long it will stay like this.

As for everything Locke found — including specific stocks he thinks you need to own before the IPOs arrive — Click here.

Bottom line: Between inflation data, Fed policy, AI disruption, and the historic IPO pipeline, investors have a lot to digest. Buckle up!

I wish you a good evening,

Jeff Remsburg

PS Louis Navellier does something I’ve never seen him do before

The legendary investor teams up with TradeSmith to unveil a new AI-powered investing approach designed to help investors become more tactical in a fast-moving market.

What’s especially interesting is that you don’t have to wait to taste the action. You can use the free pointer tool to do this Validate the stocks you already own in the short termthen joined Lewis on June 10 to attend Full width.

I’ll bring you more on this tomorrow. But to learn more now, just click here.