Listen to the audio version of this article (generated by artificial intelligence).

Micron’s profits break records… PCE inflation hits 4.1%… But what about the inflation number that Warsh is monitoring?… Are we only in the third inning of AI?

I write on Thursday micron(in) It rose 14% after the memory chip giant reported huge profits yesterday after the closing bell.

The numbers were amazing…

Revenue was $41.5 billion last quarter, up from $9.3 billion a year ago. Earnings came in at $25.11 per adjusted share, beating the $20.28 Wall Street had expected. Gross margins jumped to 84.9%, more than double what they were 12 months ago.

Then guidance came..

Micron told investors to expect revenue of about $50 billion next quarter. Analysts expected $43.6 billion. This is not a win. This is a different zip code.

The story behind the numbers is straightforward: AI is eating memory chips faster than anyone can manufacture them. CEO Sanjay Mehrotra was frank on the analyst call — he can’t say when the memory shortage will end:

Although we expect industry supply to gradually improve in 2028, we currently have no line of sight as to when memory supply will be able to catch up with growing demand.

We expect challenging conditions to persist beyond calendar 2027 as a result of AI-driven demand across all sectors coupled with structural supply constraints.

To secure this demand, Micron has announced 16 long-term supply agreements with data center operators and other key customers, each covering three to five years. Upon completion, approximately half or more of Micron’s revenue will be committed under these deals.

This is a fundamental shift for a company that has historically been hostage to memory cycles of boom and bust.

Bottom line: The AI boom is still alive and well, and despite some good profit-taking today in the technology space, the MU numbers bode well for the AI bull.

Meanwhile, the May PCE report fell this morning

It showed that headline inflation reached 4.1% year-on-year, up from 3.8% in April, the highest reading since April 2023.

Meanwhile, core personal consumption expenditures — which excludes food and energy — averaged 3.4% year over year, slightly higher than 3.3% in April.

Beware of financial media comments about Fed Chair Warsh staying hawkish and rate hikes — not cuts — as the most likely next step.

maybe. But this reaction misses something important – namely TRUE The number Warsh is tracking, which also dropped today…

And when you understand that, you’ll have a better read on Fed policy than most investors and speakers.

Warsh doesn’t primarily look at the same inflation numbers as everyone else

During his Senate confirmation hearing in April, he said the Fed’s standard measure of inflation — the one CNBC and others are publishing on their homepage this morning — is only a “rough scoop” of actual price pressures.

“Swag” means “wild scientific guess,” he explained.

Instead, his preferred measure is the so-called “Average PCE,” which the Federal Reserve Bank of Dallas publishes monthly.

This concept deserves a brief digression, because it will reshape how every inflation report is read from now on.

The standard PCE takes every item consumers buy — gasoline, groceries, streaming subscriptions, hospital visits — and averages all their price changes. This means that a one-time rise in oil prices (for example, due to a conflict in the Middle East) is included directly in the headline reading, even if the rest of the economy is pricing normally.

Now, Core PCE does a better job of addressing this issue. It eliminates food and energy prices.

But there’s a problem with Core, too – it’s still absorbing every other price spike caused by energy costs.

While it ignores rising oil prices, it will take into account, for example, the higher airfares charged by airlines to offset higher jet fuel costs. Because airfare is classified as a service, the energy shock creeps into core personal consumption expenditures through the back door – and is widely confused with inflation.

Another example: The basic personal consumption expenditures system excludes “food purchased for consumption at home” (groceries). However, it explicitly includes “food and accommodation services” (eating out) as a service.

So, let’s say you have bird flu that drives egg prices through the roof. This inflation can still show up when eating out, although it is not expressed in core personal consumption expenditures.

The solution – the measure of inflation favored by Warsh – is the “average personal consumption expenditures rate,” which takes a different approach…

It correlates all individual price changes from low to high, deletes the most extreme readings at both ends of the spectrum — temporary outliers, up or down — and then averages what’s left in the middle.

For Warsh, the result is a clearer picture of inflation actually embedded in the economy, rather than noise generated by geopolitical shocks.

To see the difference this can make, let’s go back to last month.

Core personal consumption expenditures for April averaged 3.3% year over year. However, the Dallas Fed’s average rate for the same month was only 2.35%. That’s about 1 percentage point lower — just above the Fed’s target of 2%.

This is a big difference.

So the issue today that investors should have been watching wasn’t the headline or core PCE numbers alone – it was the shrinking average number, and whether the spread between it and core PCE will narrow, widen, or stay the same.

We got the answer…

What today’s trimmed average numbers told us

A few hours after the decline in personal consumption expenditures data, the Federal Reserve Bank of Dallas published the average figure for May. The annual figure came in at 2.42%, slightly higher than April’s annual figure of 2.35%.

Find out what this means…

With core personal consumption expenditures at 3.4% this morning, the gap between it and the shrinking average (2.42%) remained at almost a full percentage point.

This is supported by Warsh’s belief that excluding price outliers reveals an underlying inflation trend that is close to the Fed’s 2% target – and remains fairly stable.

On that final note, here are the annual average numbers over the past six months:

- December: 2.4

- January: 2.4

- February: 2.3

- March: 2.4

- April: 2.3

- May: 2.4

While the hawkish camp will point to this morning’s 2.8% annual rise this morning as evidence of new short-term heat, the broader 12-month baseline proves the structural trend remains firmly entrenched.

Bottom line: This was a win on the inflation front. From now on, keep your eyes on the shrinking average – this is the number Warsh is actually watching.

Are we only 3?Third The beginning of this artificial intelligence boom?

Beyond writing digestI also run InvestorPlace Investing from within A newsletter where I feature interviews with our expert analysts, provide a glimpse into the research of major Wall Street investment shops, and highlight the most profitable investment trends in the market.

In tomorrow’s issue, I sit down with legendary investor Louis Navellier, who makes a bold claim…

The AI boom may only be in its third phase.

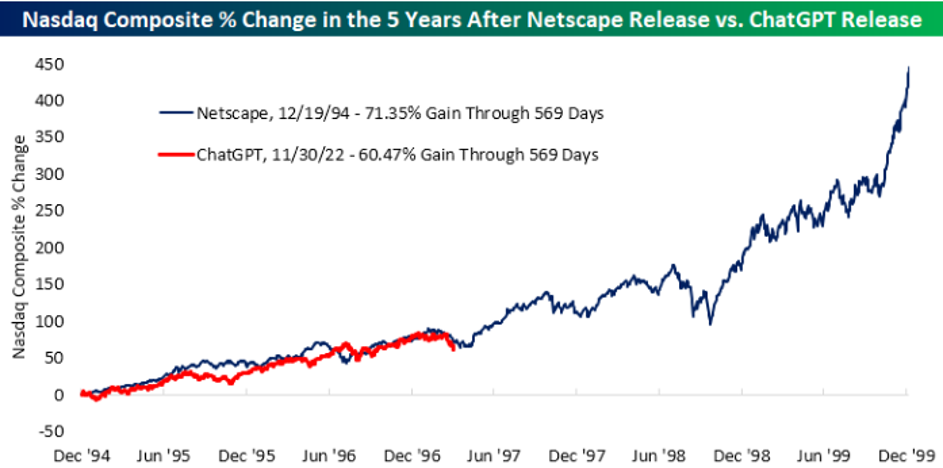

He points to a chart from research shop Bespoke that shows the NASDAQ’s trajectory after ChatGPT was released on the same window after Netscape was released in 1994.

As you’ll see below, the blue line is the Nasdaq’s performance in the five years following Netscape’s release, versus the red line – the years following ChatGPT’s launch in late 2022.

Although the data only lasts until the spring of 2025, the Nasdaq has not fallen since then. If anything, it’s that the red line has continued to rise – meaning the comparison is likely to continue to trail.

Now, the Bears might be reading this and thinking: “No, we’re already in phase niney First half, we’re on the verge of an AI bubble that will be just as brutal as the dot-com bubble.

maybe. But be sure to keep one key difference in mind…

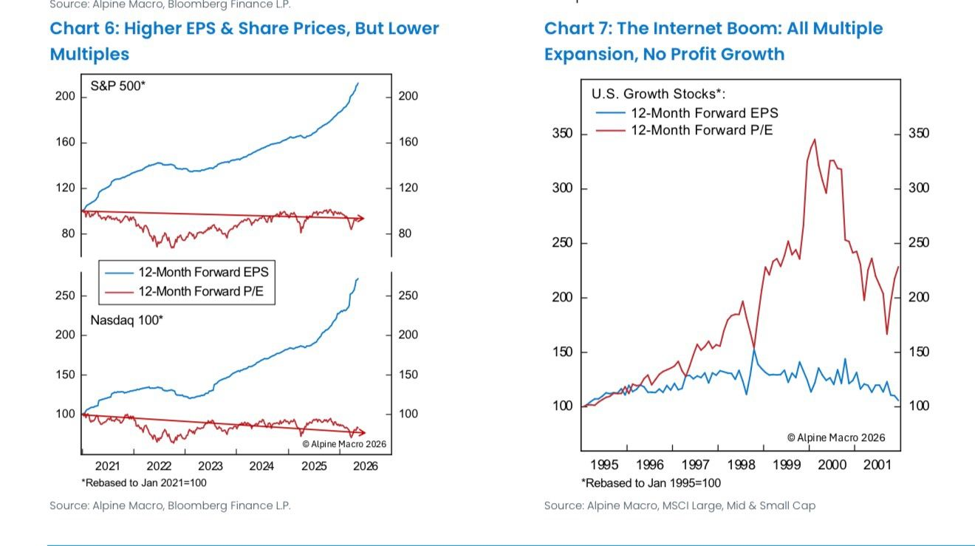

The chart from Alpine Macro shows that today’s AI boom has something of a dot-com era He didn’t do that He has…

Real earnings growth, not just multiple expansion.

In the dot-com boom, P/E ratios went to the moon while earnings barely budged. Today, earnings per share are more than doubled while multiples have remained relatively constant. This is a structurally different setup – and arguably more durable.

See for yourself…

The panel on the left shows today’s AI boom with rising forward earnings and a largely flat P/E. The panel on the right shows dot-comward’s P/E ratio rising (and then crashing) as forward earnings remained largely flat.

Source: Alpine Macro / Bloomberg Finance

However, there is one wrinkle here that is worth a closer look

There are legitimate questions about whether some of today’s AI-driven earnings growth is as clean as it seems.

A growing group of analysts point to a capex recycling loop: where highly-scaled companies like Google and Microsoft reap profits while shifting huge capex to AI startups that in turn consume those companies’ cloud and AI services.

For example, a cloud giant makes a multi-billion-dollar “equity investment” in a leading AI company like OpenAI. This leading company uses cash or newly acquired cloud credits to train and run models.

Hyperscaler then recognizes those specific credits as “new organic commercial cloud revenue” in its general income statements, which boosts its bottom line growth and boosts its stock price.

Financial filings show that just two unprofitable startups — OpenAI and Anthropic — anchor more than half of the nearly $2 trillion in future cloud backlog held by Microsoft, Amazon, Google and Oracle.

It’s not definitive proof, but it’s a real risk that we’ll be tracking closely digest During the coming quarters/years.

To watch the full interview with Lewis, You can join us Investing from within here.

And stay tuned tomorrow, when Lewis will release his latest research package. It highlights a methodology for tracking where institutional money is moving before it catches up with the rest of the market.

We’ll keep you updated on all these stories here at digest.

I wish you a good evening,

Jeff Remsburg