Listen to the audio version of this article (generated by artificial intelligence).

The FOMC decision is in… What Warsh pointed out… Why easing market inflation may be premature… The curve every new Fed chair faces…

As I write on Wednesday in the wake of new Fed Chairman Kevin Warsh’s press conference, markets are seeing a sell-off as investors process Warsh and the changes he has made at the Fed.

A quick read on Wall Street seems pretty straightforward: Warsh wasn’t as pessimistic as the market wanted him to be.

At the same time, what Wershe actually said — and what he deliberately didn’t do — tells you everything about where this presidency is headed.

Back in the day, as expected, the FOMC voted unanimously to keep interest rates at 3.5%-3.75%. But as we pointed out yesterday digestThe interest rate decision itself will not be the story today.

Question marks surround the official language of the statement, the facilitating bias, the press conference, and what Warsh did with the dot plot.

Let’s take them in order.

Statement first. Warsh not only chopped it up, he destroyed it. Today’s official release came in 132 words. The previous statement under Jerome Powell ran 344.

Warsh acknowledged the change directly at the top of his press conference:

It’s a little shorter, a little simpler, and dispenses with some of the older language. This statement gives you the facts to the best of our ability to judge.

More importantly, the accommodative bias was gone – the language that signaled the next move in interest rates was more likely bearish than bullish, one of the three things we asked you to watch for yesterday.

But Warsh went further than just removing it. All future guidance is also gone. Back to workshops:

There is also the absence of the so-called advance directive, which we agreed is not entirely compatible with the current political situation.

The era of explicit Fed guidance appears to be changing dramatically, at least for now.

As for Warsh’s tone on the podium, it was thoughtful, but he did not exaggerate his words, nor did he give much hope to the doves.

He said the committee was “unequivocally and unanimously” committed to delivering the 2% – but when reporters pushed him on future guidance, he took the bait.

He also refused to commit to holding a press conference after every future meeting, leaving that open as well.

Then there was the plot point.

Yesterday digestWe flagged this as a potential point of major change – and specifically suggested that Warsh might decline to make his own point as a deliberate first step toward deconstructing the framework.

This is exactly what happened.

Warsh confirmed this himself at the press conference:

Didn’t make a point for me. It is not useful in managing politics.

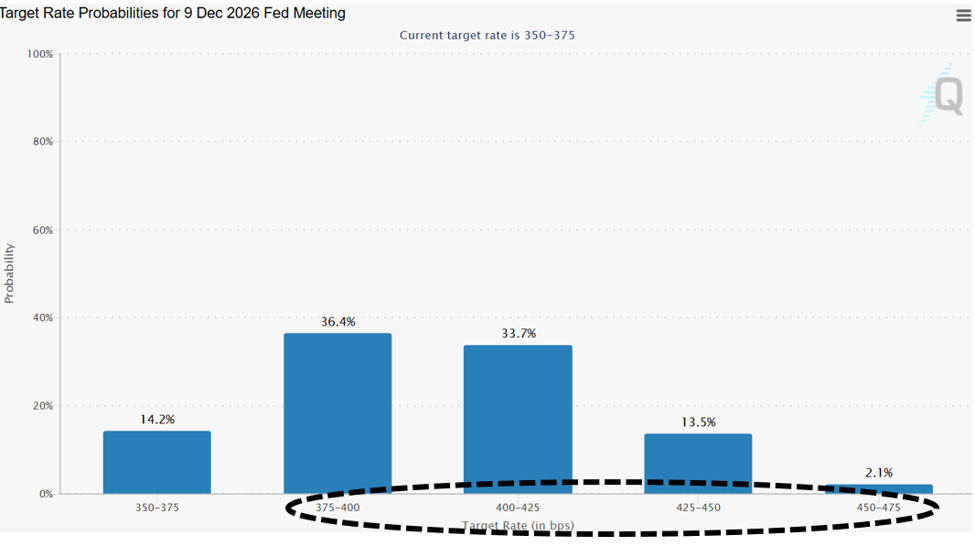

The remaining eighteen participants submitted their predictions, and the results were astonishing in themselves.

The committee is split roughly down the middle — nine officials see at least one rate hike this year, eight see no change, and one wants a cut.

The median forecast now puts the federal funds rate at 3.8% by the end of the year, up from 3.4% in March.

But with Warsh off the list, and given his publicly stated hawkish bias, the committee’s true center of gravity may lean more toward a hike than average expectations suggest.

But there was a development that we did not expect to happen…

Warsh announced the formation of five task forces that will formally review the Fed’s operations going forward — covering communications, the balance sheet, data sources, the impact of artificial intelligence and productivity, and the Fed’s inflation framework.

It is important that the points chart and the format of the press conference are clearly on the table. Warsh explained that he is interested in modernizing the Federal Reserve, as well as how it operates and communicates.

Another line from the press conference worth noting…

When asked if Fed policy was already restrictive, Warsh said:

Overall, I would say that Fed policy appears to be fairly restrictive.

It would be difficult for me to be able to say these words if I saw what was happening in the financial markets.

This is a subtle but important signal.

Warsh monitors financial conditions – not just interest rates – and does not believe markets are behaving as if monetary policy is tight. File this one away.

The market wanted caution… but it didn’t get it

Since the peace deal with Iran was reached on Sunday, markets have been moving in one direction – up.

The prevailing narrative was simple: the Strait of Hormuz had reopened, the oil shock was over, inflation was yesterday’s problem, and the Fed could now shift toward an easier policy.

Warsh has not confirmed the veracity of this account. Today’s selling is the market’s response.

But what’s worth understanding is that the market’s disappointment may say more about its assumptions than anything Warsh got wrong.

After all, the inflation problem Warsh was dealing with was never about Iran – and the peace deal with Iran was never a real solution to that problem.

Here’s what the deal actually fixes: a severe energy price shock. The price of oil rose to nearly $115 per barrel at the height of the conflict. As the strait reopens, this rise will decline. The headline inflation rate – a figure that includes energy – is expected to decline in the coming months.

On this specific point, the market’s previous optimism was rational.

But a decline in headline inflation does not mean the Fed’s problem is solved.

The Fed targets inflation in personal consumption expenditures – specifically core personal consumption expenditures, which excludes energy prices entirely. The core PCE rate has remained above the Fed’s 2% target for five straight years – through rate hikes, through pauses, and throughout the entire Iranian conflict. The peace agreement does not affect any of that.

The underlying drivers of inflation – a federal government running a $2 trillion annual deficit, utility costs that have proven remarkably stubborn, and wage growth that has not fully returned to normal – have not changed structurally.

So the expectation that a ceasefire would pave the way for interest rate cuts was always surprising.

Not convinced?

Here’s the simplest way to test pressure.

Before the Iran conflict began on February 28, the core personal consumption expenditures rate—the Fed’s preferred measure of inflation, which excludes energy entirely—was 3.1% and moving in the wrong direction, already well above the Fed’s 2.0% target.

The Iranian conflict itself, according to the Dallas Fed’s model, added approximately 0.3 percentage points to the core of the conflict at its peak. So, even if the peace deal succeeds in calming every bit of conflict-related inflation, core inflation will remain at 2.8% to 3% – well above the Fed’s 2% target, and on a path that was already stalled before Iran entered the picture.

The market was celebrating the removal of something that was never the root cause of our underlying inflation problem to begin with.

As the inflation picture returns to baseline, here’s what’s real He has change

The labor market has seen quiet improvement in recent months.

Employment opportunities per unemployed worker rose again to above 1.0. Nonfarm payrolls in May jumped by 172,000.

This is important. This means that the labor market is less fragile, giving dovish interest rates hopes for cuts.

Before the peace deal with Iran, traders were anticipating a roughly 66% chance that interest rates would rise at least once before the end of the year.

Immediately after the peace agreement with Iran, this number decreased sharply.

But today, in the wake of the FOMC decision and Warsh’s press conference? It has risen to nearly 86%.

The labor market data pushing for higher interest rates had nothing to do with Iran and did not change. The market appears to be waking up to this as it grapples with Warsh’s hawkishness.

Put it all together and here’s the end result…

The deal with Iran is really good news for headline inflation, and the market was right to price that in. But the broader inflation problem is only partly based on energy. The non-energy part is still there, still stuck, and still a problem for the Fed.

On the other hand, the fragile labor market that once held the Fed’s dual mandate in rough equilibrium is no longer so fragile.

What does this mean for Warsh?

The question he faces now is not whether the conflict is over, but whether core inflation (which was heading in the wrong direction before Iran) begins to cooperate once the energy distortion disappears, and whether the labor market continues to tighten.

These are really open questions, and the data over the next few months will answer them.

Meanwhile, the market wants what it always wants: easier policy, lower interest rates, and the Fed on its side. This is no different.

What’s different is the new Fed chairman, who on his first day gave the doves almost nothing to work with – no forward guidance, no easing bias, no point of his own, and a news conference that clearly refused to chart a course for cuts.

Today’s sell-off is the market’s handling of this reality.

His decisions in the coming months will tell us more about his presidency than anything he said today.

Coming full circle

Yesterday, we asked whether Warsh might signal – directly or through deliberate ambiguity – that the era of explicit Fed guidance is over. We got a straight answer.

He stripped the statement to its essence, refused to make his own point, asserted it publicly on camera, and launched a formal institutional review of every major communications tool the Fed has used over the past 15 years.

This is not a signal. This is a regime change, for sure.

But that’s the thing about changing the system: the first step is the easy part…

The toughest test comes when the data isn’t good – and today’s sell-off suggests the market is already feeling a gap between what it wants and what Warsh wants to achieve.

Welcome to the era of workshops.

I wish you a good evening,

Jeff Remsburg