This is a clip from The Breakdown newsletter. To read the full editions, Subscribe.

“In economics, things take longer than you think, and then they happen faster than you thought.”

– Rüdiger Dornbusch

The opening scene of Philip K. Dick in 1969 OPEC It features the apartment door that demands payment from the owner.

When Joe Chip, behind on his rent, tries to open the door for a guest, he replies: “Five cents, please.”

If there is no change, he offers to pay tomorrow, but his credit score has been downgraded so he ignores him at the door.

He tries to reason: “What I’m paying you,” he tells her, “is in the nature of a reward; I don’t have to pay you.”

“I think otherwise,” the door answers, before asking Chip to check his contract.

“You discover that I am right,” says the door. He seems arrogant.

When Chip begins to unscrew the latch mechanism with a knife, the door threatens legal action, but Chip is undeterred – “I’ve never been sued by a door before. But I think I can live through it.”

Before any damage can be done, a guest pushes Chip from the other side and finally opens the door.

Later, the refrigerator, coffee maker and shower require payment before being serviced – and the guest must pay for the door again to leave.

This was Philip Dick’s dystopian vision of the future: apartments turned into pay-as-you-go vending machines.

But this may also be the case Sh-The future of decentralized finance

The dream of DeFi is to turn every asset into a programmable financial instrument that automatically enforces the terms of its contract.

The problem with DeFi is that it is limited to crypto assets, because a smart contract cannot access the physical world to repossess a car or evict a tenant.

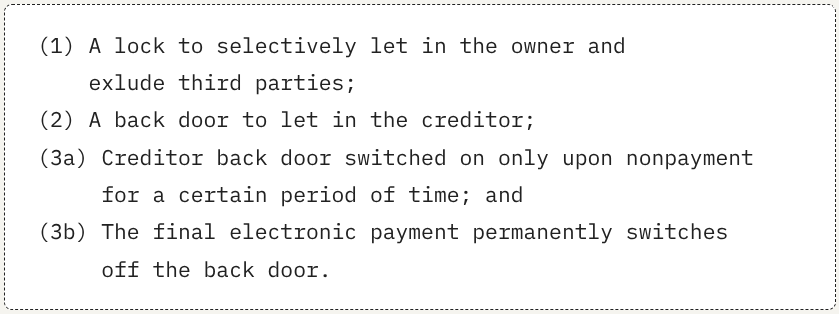

But what if a smart contract could lock the door of your house, car, or refrigerator?

In this world, a lender can accept these types of real-world assets — anything that can be locked — as collateral against on-chain loans.

It’s not a new idea.

Back in 1997, Nick Szabo described The benefit of turning smart contracts into smart locks: “Many types of contractual terms (e.g. warranties, bonds, limitation of property rights, etc.) can be embedded in the hardware and software we interact with, in such a way that breaching the contract is costly (if desired, and sometimes even prohibitive) for the violator.”

“These protocols will give control of the encryption keys to operate the property to the person who legitimately owns that property, based on the terms of the contract,” he added.

Until now, this property has only been tokens, because it is the only property whose ownership can be included in smart contracts.

But smart closingControlled by smart contracts with verifiable and immutable rules, it could turn the entire world into a vending machine.

Szabo called vending machines “the primitive predecessor to smart contracts”: a mechanical contract that holds an asset (a can of soda, for example) and releases it to anyone who fulfills the terms of that contract (inserting a coin). No need for a human store owner or company.

The rules-based machine becomes the owner of the store, just as Joe Chip becomes the owner of his house.

Szabo believed that something like the latter was where we were headed: “Smart contracts go beyond the vending machine in proposing to embed contracts in all types of valuable property controlled by digital means.”

Sixteen years before Ethereum, Szabo envisioned smart locks giving digital control of real-world property, citing automobiles as the “most obvious” use for smart locks.

“We can create a smart lien protocol: if the owner fails to make payments, the smart contract invokes the lien protocol, which returns control of the car keys to the bank.”

Nothing quite like that has happened yet, but Szabo was at least directionally correct — for two reasons: smart contracts exist, on Ethereum and elsewhere, and car loan lenders secure their collateral through remote locks.

Start interrupt devices (SIDs), which allow lenders to remotely disable a vehicle when a borrower defaults on their payments, have become popular with subprime auto lenders in recent decades.

This raises some obvious questions: What if you need the car to get to work to earn money to cover your loan? What if you’re going 80 on the highway when your lender decides to disable your car?

Unlike a go-chip door, you can’t drop coins into the dashboard of a SID-disabled car to open it. And good luck getting someone on the phone at the lender to plead your case or even make a payment.

However, you can quickly top up your payment via a smart contract, on a smartphone equipped with a digital wallet.

This is not a new idea either.

In 2015, Slock.it promised exactly the kind of digital locks Joe Chip had negotiated: “With Slock, the person renting your home pays directly to the lock itself. The lock enters into a smart contract with the renter.”

For reasons that remain unclear, Slocks never caught on, or even went into production.

(The Slock.it team may have taken their eye off the ball when their side project, The DAO, nearly sank Ethereum.)

But it is also possible that they were very early.

If so, this may finally be the right time for blockchain-based smart locks.

The infrastructure is in place: chains are fast, transactions are cheap, and front-ends are easy to use.

TradFi wants to tokenize everything: Crypto assets have flopped this year, but enthusiasm for bringing real-world assets on-chain has grown.

Investors want alternative assets: The demand for productive yield outside the shrinking world of public equities appears insatiable.

Smart contract smart locks may be the way to provide this.

Consider Türkiye, for example, where borrowers pay 5% per month On their Car loanswhich amounts to more than 100% annually – 70 percentage points above inflation.

If these loans were tokenized and governed by a smart contract that automatically disables the car when the borrower defaults, wouldn’t that attract investors from everywhere?

Larry Fink of BlackRock He said This week, “the token could significantly expand the universe of investable assets beyond the listed stocks and bonds that dominate the markets today.”

Philip K. predicted. Dick with technology. Nick Szabo wrote the guide.

Now, financing just needs to build the door to investors’ utopia.

Get news in your inbox. Explore Blockworks newsletters: