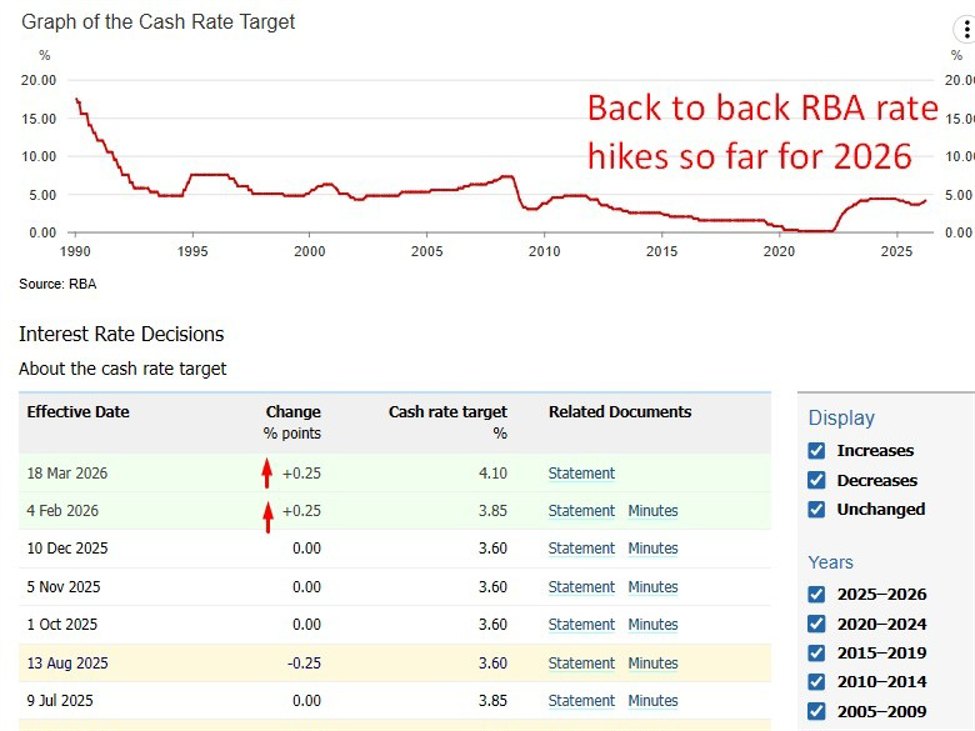

The National Bank of Australia expects the RBA to raise interest rates by 25 basis points to 4.35% on Tuesday, and updated forecasts are likely to show a final interest rate of around 4.6% as energy-driven inflation and above-potential growth limit the bank’s options.

previously:

The decision is scheduled for 2.30pm Sydney time (0430 GMT/0030 EDT)

summary:

- National Australia Bank expects the Reserve Bank of Australia to raise the cash rate by 25 basis points to 4.35% at its meeting on Tuesday, bringing the rate back to its level before the cuts implemented through 2025, according to a NAB note.

- NAB cited above-potential domestic growth, a labor market operating near capacity, and emerging inflation pressures as conditions that had already justified policy tightening before the Middle East conflict escalated, according to the memo.

- Inflation in the first quarter averaged 3.5% year-on-year, leaving the RBA with limited room to treat the energy price shock as temporary and consider its inflationary impact.

- The Reserve Bank of Australia’s updated monetary policy statement is expected to show downward revisions to near-term growth and upward revisions to inflation, with unemployment expectations little changed in the near term but revised higher, according to NAB.

- The cash rate assumption underlying the new SOMP forecast is likely to peak at around 4.6%, up from the 4.3% peak included in the February SOMP report.

The Reserve Bank of Australia is widely expected to raise its cash rate by 25 basis points to 4.35% at its meeting on Tuesday, according to National Australia Bank, with updated forecasts due to accompany the decision indicating a higher final rate than previously expected as energy-driven inflation narrows the central bank’s room for manoeuvre.

The move, if implemented as NAB expects, will return the cash rate to the level that prevailed before the RBA started cutting until 2025, effectively unraveling this entire easing cycle. NAB claims that the domestic argument in favor of tightening monetary policy was already in place before the conflict intensified in the Middle East. Growth was beyond potential, the labor market was operating near maximum capacity and inflationary pressures were beginning to emerge again. Since then the energy price shock has added another inflationary layer, raising actual inflation and near-term expectations in a way that the RBA cannot easily ignore.

Key to this assessment is the deflated first quarter inflation rate of 3.5% y/y. The trimmed average is the RBA’s preferred measure of core inflation, and a reading at this level falls materially above the bank’s target range of 2% to 3%. With core inflation already rising before the full impact of rising energy costs passes through the economy, the NAB says the RBA has limited scope to treat the current shock as temporary and keep interest rates steady.

Alongside the interest rate decision, the RBA will release its quarterly monetary policy statement containing an updated set of economic forecasts, and NAB expects these forecasts to clearly reflect the changing environment. Near-term growth forecasts are likely to be revised downward, recognizing the impact of rising energy costs and tightening financial conditions, while inflation expectations are expected to rise. Unemployment expectations are seen as broadly unchanged in the near term but rising further on the horizon, consistent with slower growth ultimately fueling the labor market.

—-

A return to 4.35% would return the cash rate to pre-easing levels, effectively canceling out the interest rate relief Australian borrowers have received until 2025, and signaling that the RBA considers the return of inflation to be too broad to accommodate.

The implied peak of around 4.6% in the updated SOMP forecast, up from 4.3% in February, is the most important figure for markets, representing a significant upward shift in the final rate assumption that will reprice mortgage rates, business lending costs and the position of the Australian dollar. With growth forecasts likely to be revised downward simultaneously, the RBA is walking into stagflation territory where neither easing nor aggressive tightening provides a clean exit. Interest rate sensitive Australian stocks and the property market face renewed pressure if SOMP confirms a longer-term higher path extending well into the forecast horizon.