Listen to the audio version of this article (generated by artificial intelligence).

Michael Burry’s Crash Warning… The Only Macro Risk That Really Matters… Why Earnings Data Tell a Different Story… Where Louis Navellier and Luc Langeau Invest Today

Michael Burry has a message for investors who have been riding this bull market…

The end… of this… is near.

Last week, Puri, the investor made famous by the movie “The Big Short,” said that “the market has skyrocketed,” and investors should “reject greed” as they consider cutting their exposure to hot AI chip stocks “almost completely.”

Here’s Puri’s general summary:

Anyone lucky enough to ride these parabolic moves, by not selling, is betting their ability to jump to or near the top…

This is all the scene of the bloody car accident, minutes before it happened.

Now, Perry is a smart guy. But that doesn’t mean he’s right.

He’s made some famous foul calls in recent years:

- His short bet against Tesla in 2021, which will very likely result in a loss…

- His one-word post on

- His position against the S&P in August of 2023 was that he had to close it because the market kept rising…

However, we would be foolish to reject his claim that we are still “minutes” away from collapse. After all, despite a “bullish” day in the market as I write on Wednesday morning, many of the most popular AI names that were hitting all-time highs a week ago are now down double digits from those highs.

Are we really a nanosecond away from collision?

Another famous investor has a different reading today – Louis Navellier.

Let’s go to his Growth investor Private Market Podcast from Yesterday:

Yields have been zigzagging higher, and that is impacting stocks.

We are seeing widespread inflation in the economy, especially due to rising shipping and travel costs.

So the concern now is stagflation – slowing growth as inflationary pressures continue to emerge.

Puri is likely to agree to this. But while Burri will continue to predict an imminent market collapse, here’s Lewis’s view:

I don’t want you to confuse today’s fluctuations with change in the bigger story. It’s been an amazing earnings season, and the AI boom remains intact…

This is what happens as earnings season ends – where profit taking begins.

There is no narrative or news causing these sell-offs…

The key question for bears who forecast a recession is: “Why now?”

That’s the thing about market crashes: they almost never happen, simply because stocks are expensive.

Evaluations can drag on for months – and sometimes years. “Expensive” has a way of increasing the cost before the reckoning comes in – often long after the collapse is expected to occur.

Older investors remember 1996, when Alan Greenspan famously warned of “irrational exuberance” in the stock market. But from this warning, the S&P 500 nearly doubled over the next four years before the dot-com bubble finally burst.

Or consider 2017, when Burri himself and a group of other sharp minds described US stocks as dangerously overvalued. The market rose another 20% before a serious correction occurred.

The point is not that warnings and high ratings don’t matter. But something has to happen Operator The unraveling of the AI business.

High P/E ratios are what light the fire – but you need to match.

“Jeff, there are millions of matches out there — Iran, oil prices, a Fed that won’t cut interest rates, tariffs, bond yields, you name it.”

justice.

But let’s look at the driver of today’s bull market — AI trading — and then look at some of these matches through the lens of AI capital spending.

From this perspective, most of today’s macro concerns appear more manageable than the headlines suggest

The reason is clear…

Ultra-fast companies have already collectively pledged hundreds of billions in AI infrastructure spending over the next 18 to 24 months. This capital is not being withdrawn due to higher oil prices or the Fed holding interest rates for an additional quarter or two.

Spending is integrated into budgets, construction schedules and supplier contracts. So, for the companies standing in the way of this spending — chip designers, data center builders, power providers — there is a well-known earnings pipeline that most macro shocks cannot derail.

Iran?

It’s painful for energy-intensive industries, for consumers at pumping stations, and for airlines. But the conflict between Riyadh and Tehran does not make Microsoft cancel its next data center.

Oil with a new home above $90?

It’s a headwind for broad corporate profit margins, to be sure — but not for the hyper-expanding capex cycle that drives AI profits.

Will the hawkish Fed keep interest rates higher for longer?

It slows down interest rate-sensitive sectors, squeezes housing, and squeezes small borrowers. It doesn’t change the competitive calculus that drives every major tech company to spend aggressively on AI infrastructure or risk being left behind.

However, there is one overall variable that cuts differently…

Bond yields.

When high yields become a problem

Bond yields are a different animal.

When 10-year Treasuries rise, it not only raises borrowing costs, but it automatically puts pressure on longer-term bond valuations. Growth stocks By making their future profits less valuable in today’s dollars.

It also gives investors a truly risk-free alternative to risky stocks. The higher the returns, the more difficult the math becomes for trading AI names at premium multiples.

Bond yields that rise too high could ultimately hurt the math behind data center loans, hindering the launch of AI.

So, where does the pain actually start?

Our technology expert, Luke Lango, editor Innovation investorhas just provided its readers with a road map to productivity.

At current levels – above 4.5% – Locke sees “some small, short-term market disruptions, but nothing more.” AI commerce remains intact.

A rise towards 4.8% to 5% would lead to “more significant disruption” – Locke suggests a 5% to 10% pullback, but nothing to break the uptrend.

Things get riskier with a 10-year interest rate above 5%.

Locke believes a 10% to 20% correction is on the table in this case. AI trading “takes a hit hard, and then bounces back faster when it recovers,” he says.

Here’s Luke with what goes further:

A break above 5.25% will start to put a damper on things.

The economy begins to crack. EPS estimates decline. Stocks fall into a bear market. AI trading is taking a hit.

A break above 5.5% will wipe out almost everything. Stock market crash of more than 30%.

As I write on Wednesday, the 10-year yield is at 4.58% – in “slightly uncomfortable but manageable” LOC territory.

So, Burri may be right that the flame is drying up, but so far, lightning strikes are still far off on the horizon.

Thwarting the risk of rising bond yields is earnings growth

There is another part of this picture that tends to get lost in the evaluation debate.

Most rating scales are retrospective in appearance by design. They measure today’s prices against yesterday’s earnings or revenues or what-have-you.

But in a high-growth environment, such a comparison brings blind spots. You’re missing out on what’s really going on now As well as what tomorrow is likely to bring – and for a large segment of this market, what ‘happens’ is an increase in profits.

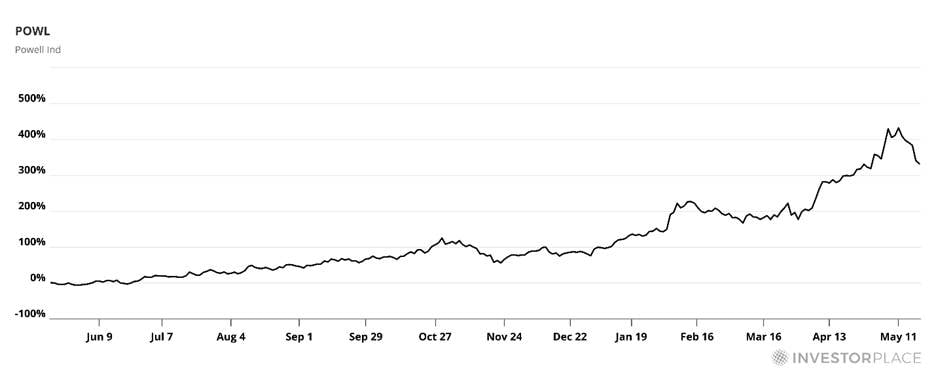

It is considered Powell Industries (Powell) – A stock I own that manufactures electrical switches and specialized power systems. It is directly in the path of building an AI data center.

As you can see below, the POWL index is up more than 300% over the past year, even after recent profit taking.

Given this price hike, a nosebleed valuation seems like a safe assumption. But it’s more complicated than that.

Depending on which financial website you visit and the earnings period it uses, POWL’s trailing P/E ratio ranges from the low 30s to the mid 50s. This is an unusually wide spread for a single stock.

What this spread reveals is that earnings have been growing so quickly that even a slight discrepancy in the chosen earnings period could produce a dramatically different picture.

There is no wrong number. They’re just measuring different versions of the same rapidly transforming business, although a P/E ratio of 33 is more accurate today.

This is the part that doesn’t appear in any P/E calculations yet…

New orders in the fourth quarter totaled $490 million, up 97% year over year. Then, after the quarter ended, one “massive order” came in from a $400 million AI data center project. These revenues have not yet appeared in the income statement. When this happens, the multiplier will be compressed further.

Backward metrics cannot capture business transformation in real time. This is the point.

Now, critics might say: “That’s just one company.” But when you zoom out, the wider picture looks the same.

This is the story today’s bears won’t tell you

According to the latest FactSet news See profits According to the report, the S&P 500 just posted its highest earnings growth rate since the fourth quarter of 2021 – 27.7% year over year, with 84% of companies beating estimates.

This beat rate is the highest since the second quarter of 2021. What’s even more surprising is that companies report earnings that are 17.9% higher than expectations — nearly two and a half times the five-year average surprise of 7.3%.

The S&P 500’s net profit margin was 14.7% – a record high since at least 2009, surpassing the previous record set just last quarter.

This is not a market that runs on fumes and hope. This is a market where profits legitimately catch up with prices – and in many cases exceed them.

Yes, beware of rising bond yields. But equally, yes, take your stock’s earnings growth into account when making market decisions.

So, what’s the verdict on Perry’s downward trends?

Puri may be right. But let’s complete our analysis with two missing pieces.

normal digest Readers will remember – and it’s noteworthy for new readers – a story we covered last November in which Puri closed his fund and returned capital to shareholders.

Why?

Because over the past two years, while Burri was anticipating and bracing for dramatic declines, the Nasdaq returned nearly 70%.

From Perry to his investors:

My judgment of the value of securities is not now, and has not been for some time, in sync with the markets.

This seems like a good time to remember the wise words of legendary fund manager Peter Lynch:

Investors have lost much more money preparing for corrections, or trying to anticipate corrections, than they have in the corrections themselves.

Puri may be right. Ultimately, some bear always is.

But the warning about stretched valuations, in the absence of a credible near-term catalyst to trigger a collapse, is not a timing call – it is market behavior. And actions don’t tell you when to sell.

What tells us something is the 10-year return, the earnings trajectory of the specific companies you own, and the durability of the capex cycle underneath.

This is the frame worth watching now—and exactly what Lewis and Locke trace back to their readers each week.

So, while Perry’s trend is bearish, here’s Lewis’ message to investors:

You basically want to buy good stocks on dips. a period.

For the latest “good stocks” he recommends investors buy on dips, You can access his latest market briefing here.

As for Luke, here is his summary:

Overall, we remain very bullish on AI trading despite the recent inflation/oil/interest rate jitters. Inflation/oil/interest rate tensions are creating just another normal pullback in a still very active AI bull market.

Commit to AI trading. Patience and determination are the name of the game now.

What got Luke excited today — what he believes could be Elon Musk’s most ambitious project yet (no relation to Tesla or SpaceX) — Click here for full view.

I wish you a good evening,

Jeff Remsburg