Listen to the audio version of this article (generated by artificial intelligence).

Alphabet says demand for AI outpaces supply…AWS posts fastest growth in four years…Meta outperforms but declines 10%…And capex sings louder than ever…Eric Fry’s latest news on where to invest in AI today

We are computer-constrained in the near term.

Our cloud revenues could have been higher if we could meet demand.

That was Alphabet CEO Sundar Pichai on last night’s earnings call — speaking directly to the question we asked Monday digest.

The numbers that followed were truly impressive – across the board. But as with most things in this AI story, there is more than the headlines suggest.

On Monday, we presented a rundown of last night’s big tech companies’ earnings not as a test of individual companies, but as a diagnosis of AI trading itself. We said there are two issues to watch: revenue, as an indication of whether AI-driven demand is actually being met, and capital expenditures, as an indication of whether the conviction for that demand is holding up.

Now that the numbers are in, here’s what we’ve learned…

Tremendous revenue growth across the board

Let’s start with alphabet (Google).

Google Cloud revenue rose 63% year-over-year to $20.02 billion — far exceeding Wall Street expectations of $18.05 billion. Total revenue was $109.9 billion versus $107.2 billion agreed upon, with net income up 81% from last year.

It was a great performance, putting Pichai’s quote above into important context. He wasn’t just talking about the usual CEO earnings optimism — he was highlighting real supply constraints.

Not only did Google Cloud, which serves as the company’s primary AI revenue engine, outperform expectations, but demand for it was limited.

From Pichai:

Our enterprise AI solutions became the primary driver of cloud growth for the first time in the first quarter.

This is a stronger signal for enterprise AI demand than public cloud growth – but I would point out that it is still closer to the infrastructure layer than an end-user monetization signal. I’ll talk more about this distinction soon.

Switch to Microsoft (MSFT), Its revenue was $82.89 billion, versus the $81.39 billion expected, with adjusted earnings per share of $4.27, versus the estimate of $4.06. Azure and other cloud services grew 40% — beating analysts’ range of 38.8% to 39.3%.

Another strong performance.

Meanwhile, the institutional adoption numbers are staggering. GitHub Copilot now has more than 26 million users, and more than 90% of the Fortune 500 use Microsoft 365 Copilot. Commercial bookings jumped 112% year over year, driven by OpenAI’s Azure commitments.

Turn to Amazon (Amzn)It provided the most dramatic acceleration of the group.

Amazon Web Services (AWS) grew 28% to $37.59 billion — the fastest pace in 15 quarters, compared to 24% last quarter. Total revenue of $181.52 billion beat the consensus of $177.3 billion, and earnings per share of $2.78 overwhelmed expectations of $1.64.

One number to highlight is Amazon’s chip business. Graviton, Trainium and Nitro have now collectively surpassed the $20 billion annual revenue run rate, driving triple-digit year-over-year growth.

finally, dead (dead) Beat on revenue – $56.31 billion vs. $55.45 billion expected, up 33% from prior year and fastest quarterly growth since 2021. Additionally, adjusted EPS of $7.31 beat estimates of $6.79.

However, shares are down about 10% as I write on Thursday because the number of daily active people has reached 3.56 billion, below the 3.62 billion expected on Wall Street and more than 5% below Q4.

The company attributed this decrease in part to the Internet outage in Iran, which is a real factor. Whether this fully explains the error or hides something more structural is a question worth watching over the next quarter or two.

Enterprise growth is real, but here’s what it does and doesn’t tell us

Across all four companies, demand is strong and accelerating – but it pays to be precise about the nature of that revenue.

A large part of it relates to enterprise AI deployment: companies pay to build, train, and operate AI systems. This is really encouraging and more advanced than it was two quarters ago.

But corporate demand is also a chaotic signal…

Some of what drives these numbers is perpetual publishing. Some of them are still being tested, pilot programs and capacity building ahead of demand which has not yet fully arrived. At this point, earnings don’t clearly separate those results.

In either case, the “end user” here is mostly a company. This is a completely different story from ordinary people opening their wallets to buy AI products in their daily lives.

This market — the average Joe deciding every month whether an AI subscription is worth keeping — is still largely unproven at scale.

So, what’s our best window into this demand?

OpenAI remains the clearest window on the consumer side

It doesn’t report earnings, but as we covered on Tuesday, OpenAI missed internal usage and revenue targets due to massive computing costs and increased competition.

It has a real and growing enterprise business – ChatGPT Enterprise, API revenue, and deep integration with Microsoft’s product suite. But consider the scale of its infrastructure commitments: OpenAI has committed itself to spending $250 billion on its Azure service alone — and that number doesn’t even include the broader computing costs its operations require.

At this scale, even strong enterprise growth may not be enough to close the loop. Consumer monetization isn’t a nice-to-have – it’s a necessity.

Evidence of its widespread reach is still weak. This is the gap that last night’s strong institutional numbers did not resolve.

Moving on to our question about capital expenditures: The canary not only survived, it sang louder

We said on Monday that the “canary” worth watching is whether any of the super-expanders quietly signal doubt by pulling back on investment. That wasn’t our forecast last night – we’ve marked the Capitalist Canary as a long-term watch, not an imminent threat.

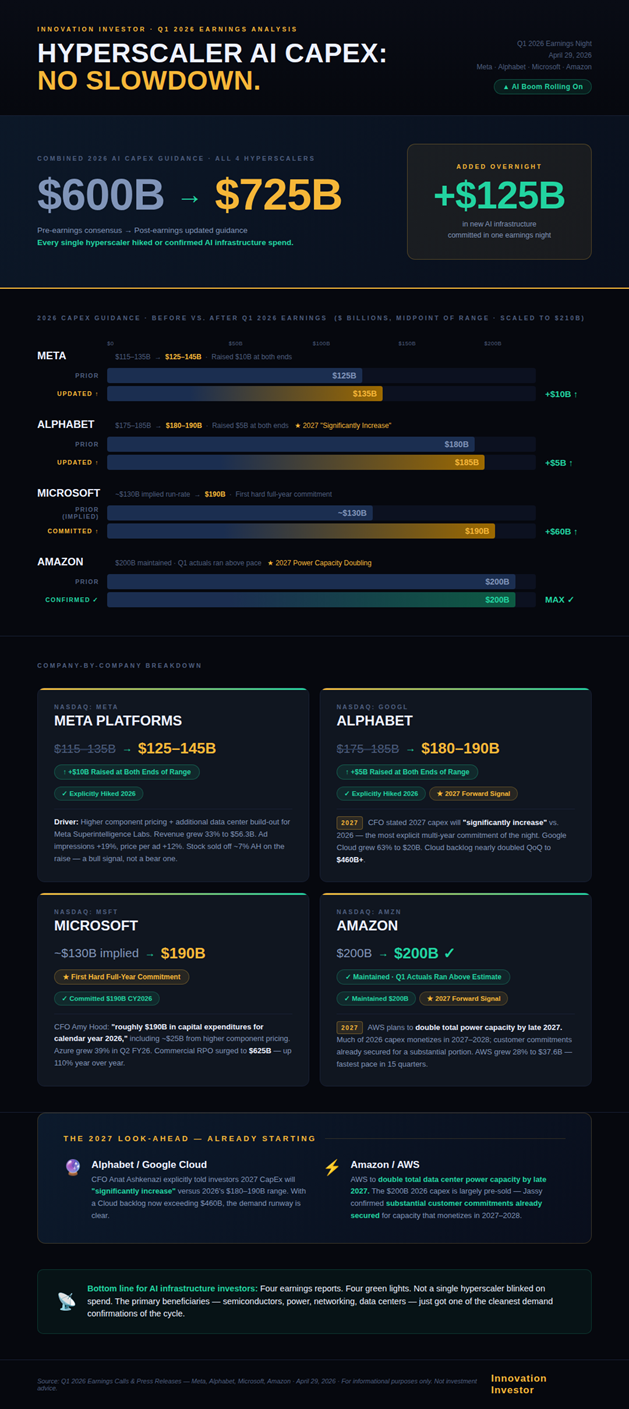

But wasn’t there even the slightest glimmer of that sign: three of the four countries raised their spending commitments, and the fourth stuck to a $200 billion plan for the full year.

In fact, Microsoft’s quarterly capital expenditures came in below estimates — $31.9 billion versus the consensus of $35.3 billion — but coupled that with full-year guidance of $190 billion, well above the $154.6 billion that analysts had expected. The message: More condemnation overall, just at a more deliberate quarterly pace.

Alphabet raised its full-year range to $180 to $190 billion, up from $175 to $185 billion previously, and CFO Anat Ashkenazi told analysts they expect 2027 capital expenditures to rise significantly from there.

Meta raised its range for 2026 to $125 to $145 billion, from $115 to $135 billion, due to higher component prices.

Finally, Amazon is sticking to its $200 billion commitment.

Add that up, and you’re looking at up to $700 billion in combined capex for 2026 across these four companies.

This is not just a vote of confidence in the potential of AI, it is a hundreds of billions of dollars bet that the demand is real and growing.

Here’s a chart sent to me by our hypergrowth expert, Luke Lango, that sums up the numbers:

Bottom line: The capital expenditure picture is becoming increasingly clear. The returns image is where it gets more precise.

So where does all this leave us?

In a better place than skeptics expected, but in a more nuanced place than the bulls might admit.

The infrastructure layer delivered really good news last night. Demand for the cloud is real, accelerating, and in some cases supply-constrained — even if it doesn’t clearly tell us how much of that demand will translate into permanent monetization for the end user.

But what we didn’t learn last night is whether the current wave of enterprise AI adoption is primarily a cost-cutting story from Corporate America or the beginning of a real new revenue generation story.

Right now, the evidence leans toward efficiency: companies using AI are doing more with fewer people. This is valuable. But cost cutting has a ceiling.

What we would rather see is AI generating entirely new revenue streams rather than cutting existing costs – something that is not yet clearly visible in the numbers.

Bottom line: Last night’s numbers were strong. They confirmed that the bet on infrastructure is real. What they haven’t done is prove that the returns will match the investment.

Which brings us to the question: Does the $700 billion capital expenditure figure raise…

If construction companies are spending this much, who actually gets the return?

Our global expert Eric Fry Speculators He has spent months studying how major technological breakthroughs happen – and his conclusion adds a layer of complexity to last night’s numbers.

His research shows that in every major technology cycle, from railways to the Internet, it is rarely the infrastructure builders who get the lasting gains.

As Eric says:

The builders struggled. Applicants became wealthy.

He points to Cisco – the poster child of Internet infrastructure – which lost nearly 85% of its value after the dot-com bubble burst and took decades to recover.

Which company used Cisco debris best?

Amazon – up over 100,000% since its early days.

Eric believes the same rotation – from AI Builders to AI Appliers – has now begun. In his new free presentation, he names stocks he’ll sell and overlooked companies that he believes represent the next step.

To come full circle, we’ll finish this…

AI trading is real. Whether it is as profitable as it is powerful is the question that will define the next few years.

I wish you a good evening,

Jeff Remsburg