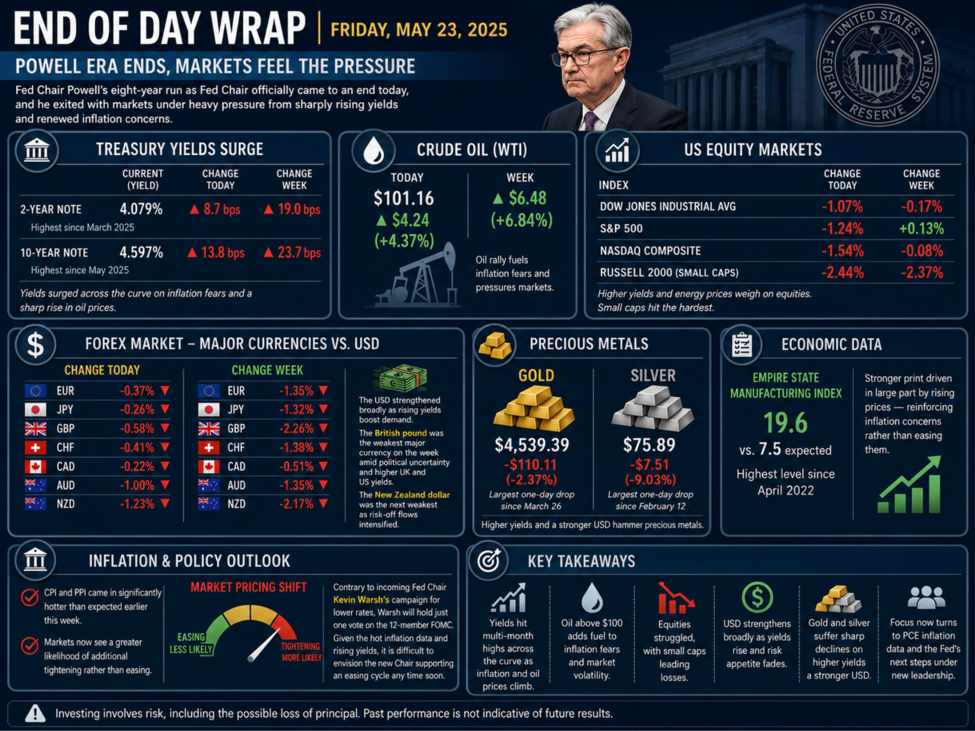

Fed Chair Powell’s eight-year term as Fed Chairman officially ended today, and he exited with markets under intense pressure from a sharp rise in yields and renewed concerns about inflation.

US Treasury yields rose across the curve. The two-year bond yield rose 8.7 basis points on the day and 19.0 basis points for the week to 4.079% – the highest level since March 2025. Meanwhile, the 10-year bond yield rose 13.8 basis points today and 23.7 basis points for the week to 4.597%, the highest level since May 2025.

The main driver behind the move was another sharp rise in oil prices, which continued to stoke inflation fears. West Texas Intermediate crude for July delivery rose $4.24, or 4.37%, to settle at $101.16. Over the course of the week, the price of crude oil rose $6.48, or 6.84%, raising concerns that inflation pressures may remain elevated for longer than markets expected.

US stocks did not respond well to the combination of higher yields and higher energy prices. Major indexes gave up much of their weekly gains in Friday trading. The Dow Jones Industrial Average fell -1.07% on the day and ended the week down -0.17%. The S&P 500 fell -1.24% on Friday but posted a modest weekly gain of 0.13%. The Nasdaq fell -1.54% on the day and fell -0.08% on the week.

Small-cap stocks were particularly hard hit, as rising yields pressured growth and financing expectations. The Russell 2000 fell -2.44% on Friday and ended the week down -2.37%.

In the Forex market, the US dollar strengthened broadly as rising yields boosted demand for the US currency. All major currencies fell against the dollar today:

-

EUR -0.37%

-

Japanese Yen -0.26%

-

British Pound -0.58%

-

Swiss Franc -0.41%

-

Canadian Dollar -0.22%

-

Australian Dollar -1.00%

-

NZD -1.23%

During the week, the British pound was the weakest of the major currencies amid political uncertainty and a sharp rise in UK and US yields. The New Zealand dollar was the next weakest as risk-off flows intensified:

-

EUR -1.35%

-

Japanese Yen -1.32%

-

British Pound -2.26%

-

Swiss Franc -1.38%

-

Canadian Dollar -0.51%

-

Australian Dollar -1.35%

-

NZD -2.17%

Precious metals were also hit hard by a combination of rising yields and a strong US dollar. Gold fell $110.11, or -2.37%, to $4,539.39 – the biggest one-day drop since March 26. Silver fell $7.51, or -9.03%, to $75.89, marking the largest daily decline since February 12.

On the economic front, the Empire State Manufacturing Index came in much stronger than expected at 19.6 versus 7.5 expected, reaching its highest level since April 2022. However, much of the strength appears to be tied to rising prices, which reinforces rather than eases inflation fears.

Earlier this week, consumer price index (CPI) and producer price index (PPI) inflation reports came in much hotter than expected, raising concerns that upcoming personal consumption expenditures inflation data may also surprise to the upside. As a result, market prices have turned significantly, with traders now seeing greater potential for further tightening rather than easing.

The shift runs counter to comments from incoming Fed Chairman Kevin Warsh, who called for lower interest rates while campaigning for the role under President Trump. However, once he sits at the Fed, Warsh will cast just one vote on the 12-member FOMC panel. Given the recent inflation data and the sharp rise in yields, it is difficult to imagine the new president supporting a rate cut in his first policy meeting.