Listen to the audio version of this article (generated by artificial intelligence).

Tom Young here with today Smart money.

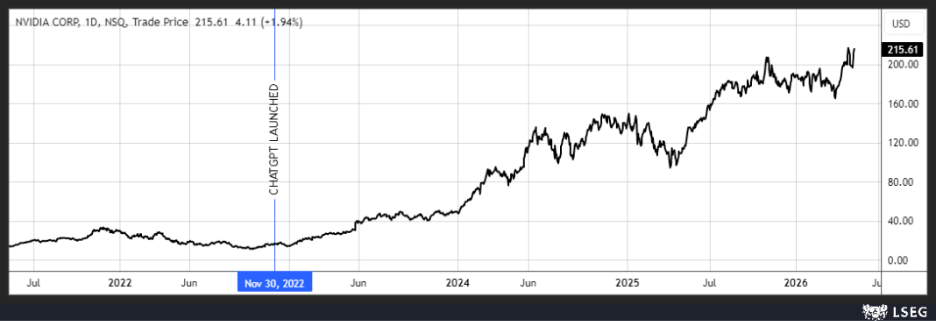

When OpenAI launched ChatGPT in late 2022, shares soared Nvidia company (NVDA) He did almost nothing for months. Like a lazy old dog, the stock price remained at $17, even as millions of users downloaded the AI-powered chatbot.

But then, NVDA started to rally.

$20… $50… $150…

The old dog learned new tricks.

By 2026, the stock had risen to over $190 — an 11-fold return in four short years. Investors have belatedly realized how many graphics processing units (GPUs) ChatGPT and its competitors will need, and how important Nvidia is as a GPU supplier.

Nvidia company (NVDA) Share price

Source: LSEG

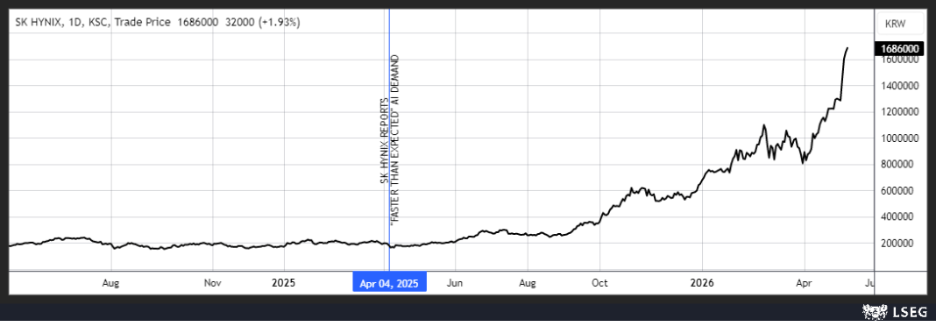

The same thing happened with shares of SK Hynix Inc., one of the largest producers of memory chips. Investors showed only moderate interest in the South Korean company until 2025… and then bought shares in late 2025 after memory chip prices began to rise due to demand for artificial intelligence.

SK Hynix share price

Source: LSEG

These two companies are not alone. Advanced Micro Devices (AMD)… Intel Corporation (Intech)… Arm Holdings PLC (arm)…Almost everyone AI shares They had a “hockey stick” moment. Stocks moved sideways until Wall Street hit some AI-related shortages. The stocks then shoot up, creating the classic hockey stick pattern we see now.

Many investors owned these companies before they were hacked. Eric himself made a triple-digit return on AMD on its flagship stock-picking subscription service, Fry investment report.

Others were less fortunate – either missing out on the AI boom entirely or benefiting only through broad-based pension funds.

Either way, everyone I know seems to be asking themselves, “Why didn’t I buy more when I had the chance?”

Fortunately, you still can.

Today, there are still a few companies that resemble Nvidia in late 2022 and SK Hynix in mid-2025. These companies produce critical components for AI data centers, and their prices are undervalued simply because Wall Street has not yet realized the shortage that will be caused by the demand for AI data centers.

per day Smart moneyI would like to highlight three of these companies. Next, I’ll share with you where you can find more of these overlooked picks.

Buy AI Stocks #1: Support the AI Revolution

AI data centers are power-hungry animals with somewhat inconsistent appetites. During the day, these AI specialists work at full capacity to answer user queries and perform AI inference tasks. This consumes huge amounts of electricity for computing and cooling. In the evening, demand decreases

This brings me to my first recommendation regarding AI:

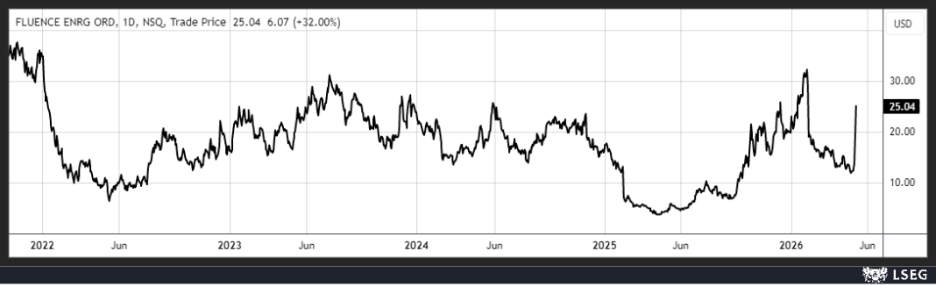

Fluence Energy Company (National Liberation Front)

Fluence was created in 2017 as a joint venture between Siemens and AES. The pitch was clear and straightforward: The two companies recognized that renewables were becoming a major part of the grid’s output, and that utilities needed to store energy when the wind didn’t blow and the sun didn’t shine. Fluence was created to sell bulk batteries and specialized software at scale.

The company is now at the forefront of AI data center power.

Earlier this week, management announced that demand doubled to $2.0 billion from a year earlier, thanks in large part to demand for data centers. The company is now in discussions covering 36 GWh of projects – enough to provide more than two dozen hyperscale AI-powered data centers with the backup power they typically need. There is likely to be more growth on the way as AI data centers begin building their own power plants to address grid shortfalls. (These small power plants often need… more Balancing the load from the batteries because they are not connected to a larger grid.)

This will have an incredible impact on Fluence’s growth. Revenue should rise 47% this fiscal year and 23% the next, turning the company’s $48 million loss in 2025 into a $30 million profit by 2027… and then $100 million a year after that.

Fortunately, Fluence’s recent rally reflects only part of this uptrend. Shares are still trading well below their IPO price despite a 28% rise in earnings this week. For the growth-seeking investor, Fluence Energy is an attractive combination of growth potential and affordable pricing.

Fluence(National Liberation Front) continues to trade below its IPO price

Source: LSEG

AI Stock to Buy #2: AI Channel

Hyperscale AI-powered data centers can require thousands of miles of cabling. A single Nvidia NVL72 rack uses approximately 5,000 NVLink copper cables — wrapping several miles of stuff into an average-sized cabinet. There are also medium voltage cables to operate servers, high voltage cables for cooling systems, and others.

This leads me to my next choice:

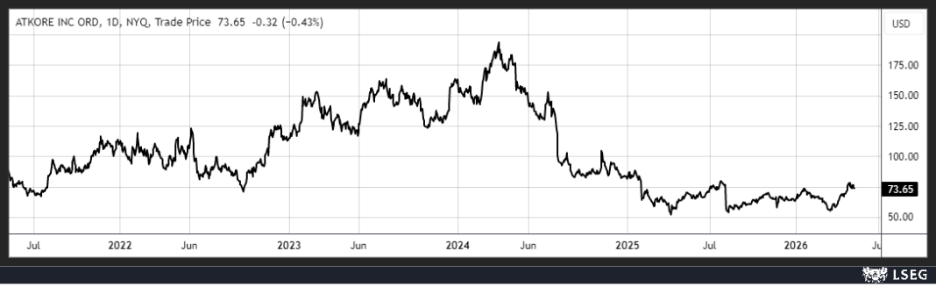

Accor Company (ATKR).

Atkore is an American manufacturer that builds power system products. These include conduits, cable management products, metal frames, mechanical piping and other “behind the wall” items that keep electricity and data flowing.

The company has enjoyed unusually strong profitability during the post-pandemic construction boom. Shares rose fivefold to nearly $200 between mid-2020 and early 2024 as revenue and profits swelled. Homeowners and electricians were paying large sums of money to complete home renovation projects.

ATKR then collapsed again in 2025 after construction demand dried up. Shares have now fallen to the $70 range.

This brings us an unusually good price opportunity. Management expects revenues to start growing again this year, thanks to double-digit growth in demand for data centers and renewed solar projects. Earnings growth should soon catch up in fiscal 2027.

This makes Atkore a potential hack hiding in plain sight. Analysts still price the company as a cyclical housing play. In fact, it’s a company that has been facing increasing demand as AI data centers go live for several years.

atcor (ATKR) Stocks remain low, even as demand for AI rises

Source: LSEG

AI Stock to Buy #3: The “Eyes” of the AI Revolution

Wall Street already knows that self-driving cars and robots are the next frontier of the AI revolution. Humanoid robotics company Figure AI was valued at $39 billion in private markets last year, and Google’s self-driving unit, Waymo, was priced at about $126 billion in a 2026 funding round.

But how do these cars and robots “see” the world?

The answer here is my third choice:

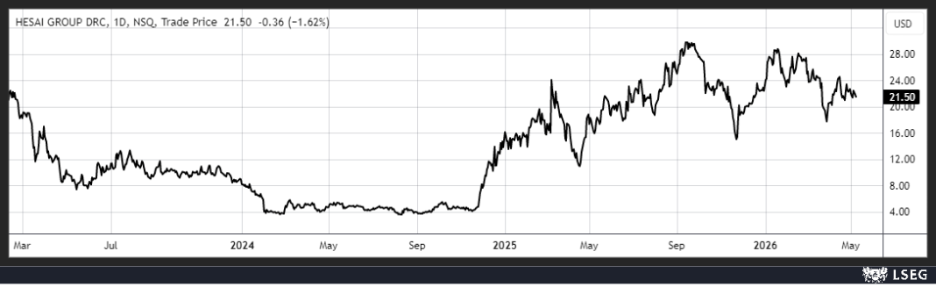

Hisai Group (HSAI).

Hesai is the Chinese technology company that dominates the market for lidar systems, devices that autonomous electronics use to sense the world around them. The company supplies more than 60% of the global taxi market, all 10 of China’s largest car manufacturers, and 40 other car brands worldwide. They are also the primary lidar partner for Nvidia’s DRIVE Hyperion 10 platform – the autonomous driving system developed by the chip maker. It is a high-volume business that has already turned Hesai into a profitable entity.

The Chinese company is also seeing growth through robotics, specifically humanoid robots and self-driving lawn mowers. The company shipped nearly 240,000 robotic lidar units in 2025, and expects that number to at least double this year.

This would add further growth to Hisai’s already rapid rise. I expect revenue to increase at least 43% this year and 40% the next, which should nearly double earnings per share to $6.35 by 2027.

Additionally, US investors are relatively unaware of Hesai, given that it is a Chinese stock that has spent most of the past three years below its IPO price.

As SK Hynix explains, these mismatches usually don’t last forever. At some point, American investors will realize how much the lidar market has strengthened under Hisai. If the pace of self-driving vehicle deployment leads to shortages of these devices, those sitting on the sidelines will feel like Nvidia in 2023 all over again.

Hisai (HSAI) has remained limited in scope since 2025

Source: LSEG

The next stage of the AI revolution

These three companies have the same thing in common:

They have traded largely sideways even as demand for artificial intelligence accelerates.

The mismatch can persist for a while. Profits can increase without stock prices going anywhere. This is called “price/earnings pressure”.

But eventually, this pressure turns into a coiled spring.

One of the best examples of this is an AI-focused payment processor Fry investment report. Since 2020, this high-quality company’s earnings have risen steadily, even as its stock price has declined.

The result is that shares are now trading at less than 9 times forward earnings… less than 50 times in 2021. This is happening even as this company expands into AI-related payment processing. You will soon be able to purchase products through ChatGPT using your Wallet with that chosen company.

Another top pick for Eric is an AI company He is the job. The company has built what is arguably the world’s most advanced AI-powered system for grading electronics, and this fast-growing business trades at just 12 times forward earnings.

Just yesterday, Eric released his monthly report Fry investment report May issue. In this issue, he explains how the next big winners in AI may not be companies that build AI models, but companies that apply AI more effectively in the real economy.

He also recommends purchasing a new product to survive in the era of artificial intelligence.

Until next time,

Thomas Young, CFA

market analyst, Investor location