As I write on Wednesday, stocks continue to rise yesterday, driven by positive geopolitical headlines.

This morning, President Trump posted on Truth Social that the Iranian president has requested a ceasefire — adding that the United States will only consider the proposal when the Strait of Hormuz is “open, free and clear.”

Meanwhile, the UAE is reportedly preparing to help open the strait by clearing it of mines, while also encouraging neighboring Gulf states to join the effort.

here The Wall Street Journal:

Emirati diplomats have urged the United States and military powers in Europe and Asia to form an alliance to forcefully open the strait.

Saudi Arabia and the other Gulf states are now turning against the Iranian regime and want the war to continue until it is disabled or overthrown.

All in all, it is enough to keep optimism high and market gains are coming. The S&P 500 has risen about 3.5% over the past two sessions as oil prices fell — a welcome relief after one of the toughest periods of the year.

Let’s step back and get some perspective

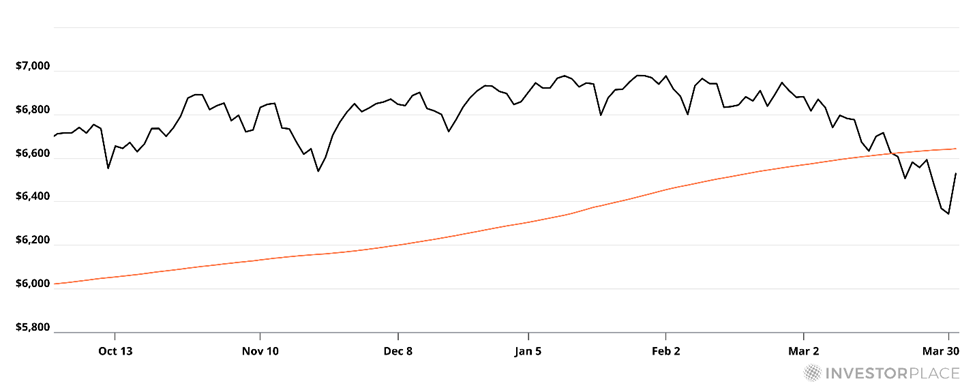

Even with this two-day bounce, as I write now, the S&P remains about 6% below its January peak. The Nasdaq and Dow Jones — which have temporarily crossed into official correction territory — are still down about 9% and 7%, respectively, from their highs.

As you can see from the chart below, even after the two-day bounce, the S&P 500 is still trading below its 200-day moving average (Master’s).

Here’s how Brian Hunt, editor of The Free Email Money and mega trendsdescribed the importance of being below the 200-day moving average in last Friday’s edition:

Stocks, ETFs, and indices that are below the 200-day moving average are “standing on the wrong side of the tracks.” It’s the ugly part of town.

All the really bad things — crashes, panics, and terrible bear markets — happen below the 200-day moving average.

But look again at the chart, and you will see that the S&P is looking to reclaim this key technical level.

Will it penetrate the market and continue to strengthen? Or will the S&P be rejected and start falling deeper?

Brian points out that today’s fundamentals, valuations and interest rates are not driving the recent price action in the broad market. This volatility is due almost exclusively to Operation Epic Fury and President Trump’s social media posts.

Therefore, he sees a simple binary that could influence the 200-day MA test:

If the war ends soon, it is very likely that the S&P will rise and return to the right side of town.

If the war does not end soon, the reduction in supplies of vital resources will cause serious damage to the global economy and stock prices will fall.

Bottom line: The last two days are encouraging. But the decision is still unclear – as we noted in yesterday’s report digestEven a ceasefire does not lead to the automatic reopening of the Strait, which would have the greatest impact on oil prices, and thus inflation, interest rates, and the rest of the dominoes.

Brian publishes his free email newsletter every day the market is open. If you’re interested in learning more about the big trends driving the market today, Sign up for Money and mega trends here.

Now, even amid this uncertainty, our hypergrowth expert Luke Lango, editor Innovation investorbetting on a bullish outcome.

The case of Luke the Bull: Why he thinks this rally could have real legs

Even with the market below the 200-day moving average, Luke sees a compelling setup beneath the surface — especially for technology and AI investors.

Some convergent signals are observed. First, market breadth has deteriorated to levels historically associated with correction bottoms – the kind of readings that in past sessions represented the area of maximum imbalance between price and fundamental value.

Meanwhile, fear indicators are pressing from their peak, suggesting that the worst of the uncertainty may already be priced in.

Corrective mathematics in itself is encouraging. Locke’s research found that every market pullback since 1950 that was capped at 10% to 20% had an average six-month return from the low of about 24%.

But the most optimistic part of Locke’s argument is the recalibration of valuation in technology specifically. Here is a look from his latest work Investing in innovationQTor Daily notes:

Valuations for technology stocks have reset to truly compelling levels relative to their proven earnings growth trajectory.

The S&P 500’s technology sector forward earnings multiple has been compressed to 20.5X — essentially a post-coronavirus low, and above where technology stocks bottomed in the 2022 bear market.

Over the next three years, technology profits are expected to grow at a compound annual growth rate of 25%. So, at current levels, investors are paying 20x forward earnings for ~25% compound earnings growth.

This is a very attractive setup.

What Luke concludes is that although we may not be quite at the low, waiting for a crystal clear signal could mean missing out. As he put it, we are “at the bottom enough.”

Now, moving on from the obvious impact of the Iran war on Wall Street, there is a new, related issue that could be a black swan ahead…

A new brewing risk to AI trading

While all eyes are on oil and the Strait of Hormuz, a quieter supply chain story is developing that AI and technology investors should follow closely.

Helium.

The same invisible gas that keeps party balloons aloft is also needed to cool the machines that make AI chips — and right now, nearly a third of the world’s supply is offline.

Iranian strikes on the Ras Laffan LNG facility in Qatar earlier this month didn’t just disrupt natural gas. They disrupted helium production lines that could take up to five years to repair.

Qatar supplies about a third of the world’s helium needs, almost all of which passes through the Strait of Hormuz – which remains paralyzed despite two days of Wall Street celebrations.

here contractor on monday:

Without helium, leading chipmakers, including TSMC, Samsung and SK Hynix, may have difficulty keeping production going.

Helium cools the superconducting magnets during chip manufacturing and removes toxic residue after the chips are washed.

The gas is indispensable in making the chips that power Nvidia’s iPhones and AI servers.

There is no easy alternative here. Helium’s unique combination of thermal conductivity, chemical inertness and atomic size makes it irreplaceable in chip manufacturing.

The Semiconductor Industry Association acknowledged this in a 2023 report to the US Geological Survey, warning that supply disruptions “will likely cause shocks to the global semiconductor manufacturing industry.”

Although some headlines suggest helium reserves “for months”, the stock picture is more dire than it seems. Containing gas is known to be difficult. said Lita Shawn Roy, President and CEO of TECHCET, a semiconductor materials consulting firm American Scientific:

Helium can leak 0.1 to 1 percent per month, depending on how good the gaskets are. There is never a good gasket or installation. It only seeps out over time.

On the other hand, about 200 specialized refrigerated containers used to transport liquid helium – each worth about $1 million – were stranded near the strait when the war began.

Industry consultant Phil Kornbluth said The Wall Street Journal Repositioning, repackaging and delivering those containers alone could take months.

Here is his comprehensive evaluation:

There’s a tsunami coming, but it’s still thousands of miles from shore.

So where could that tsunami hit?

From major chip makers, Samsung and SK Hynix Show the most exposure. Both rely heavily on diagonal width and are important products of high-bandwidth memory (HBM) inside Nvidia’s AI servers.

Taiwan Semiconductor Manufacturing Company (TSMC) It holds its own exposure as the foundry behind the chips nvidia (NVDA). Meanwhile, micron(in)with more diversified sources, looks better positioned in the near term, but still has exposure.

But the helium story also has an unexpected winner hiding in plain sight: Exxon Mobil (XOM).

Its Schott Creek facility in Wyoming represents approximately 20% of global helium production capacity and has had an 80-year reserve runway. like 24/7 Wall Street He noted that the shortage “gives Exxon the opportunity to expand its profit margin at low effort at a time when demand for chips for artificial intelligence continues to rise.”

For investors who already hold XOM for an oil and gas basis, the helium angle makes it even more interesting. For new money, it’s worth putting on your radar.

The main variable, as with everything now, is time. A quick ceasefire solves this problem before it becomes critical. But a prolonged conflict turns a distant tsunami into a very close wave.

We will keep you updated.

Finally, another round of layoffs — and an even bleaker question for AI investors

By now, most investors are aware of AI’s threat to jobs. It’s the story everyone is watching.

But there is a less discussed question that is beginning to surface, and it is one that I will address in more depth digest almost. It goes something like this…

What if AI ends up being as disruptive to most AI companies as it is to the workers they replace?

It is considered oracle (ORCL)…

Yesterday, the software giant announced a new round of layoffs — TD Coin estimates between 20,000 and 30,000 workers — though at the same time it is aggressively increasing spending on AI infrastructure. Oracle committed a staggering $455 billion in performance commitments remaining after its OpenAI agreement, all while reshaping the company around building AI.

However, ORCL stock is down 25% this year. Part of that reflects investors’ concerns about cash flow amid rising capital expenditures. But another part reflects something more troubling…

The market is beginning to wonder whether generative AI threatens not only Oracle’s employees, but its core business as well.

This question extends beyond Oracle

It gets to the heart of the entire AI investing thesis…

If AI turns intelligence into a commodity, who will actually win?

Companies that build it?

Companies that publish it?

Or maybe no one?

Perhaps more worryingly, what about the investors who currently own companies that now appear to be winning?

And the latter answer — owning the infrastructure layer, the picks and shovels, and the Nvidia hardware of the world — has served investors well. And it’s likely to continue that way… for a while, at least.

But this thesis rests on one assumption: that demand for AI computing will continue to grow indefinitely. However, what happens if the economics of AI start to work against this assumption?

What if we start a race to the bottom that will eventually trickle down to the infrastructure layer as well?

This is a bigger conversation than we have space for today. But it’s coming.

For now, here are our takeaways

That Oracle is cutting tens of thousands of jobs while simultaneously betting $455 billion on AI infrastructure is hardly a contradiction. This is what a real-time AI architecture reset looks like.

Technology is reordering how businesses are built, staffed and financed – and it’s still in its infancy.

Yes, the short-term headwinds are real…

There are potential supply shocks like helium… and unresolved geopolitics… and the S&P is still on the wrong side of the 200-day moving average. These are meaningful speed bumps.

But as Locke reminds us, investors are currently paying 20x forward earnings for roughly 25% compound earnings growth in the technology space. Whatever the road ahead looks like, it is an attractive place.

I wish you a good evening,

Jeff Remsburg

(Disclaimer: I own MU.)