Japan’s services sector is still expanding but losing some momentum, with weak demand growth, rising energy-related costs, and a sharp decline in business confidence pointing to a more uncertain outlook.

summary:

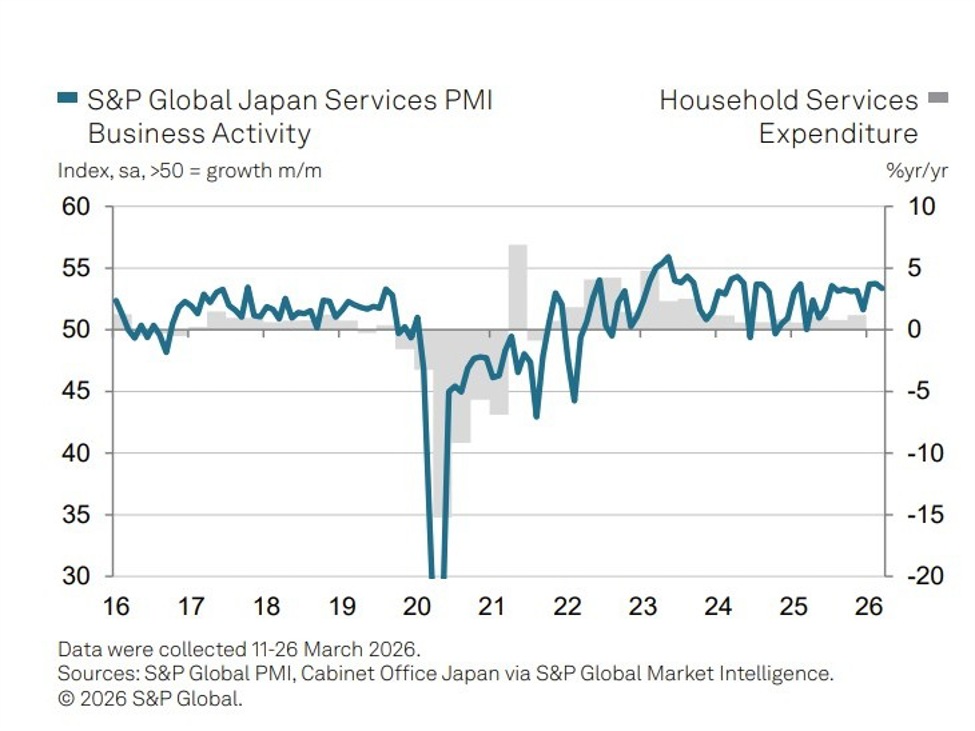

- Japan’s services PMI fell to 53.4 (previously 53.8), still a strong expansion

-

Growth in new orders slowed to a three-month low

-

Cost pressures are intensifying, driven by energy and conflict in the Middle East

-

Selling price inflation remains high but is declining from the peak

-

Business confidence falls to its lowest levels since the pandemic

-

Employment growth declined amid weak demand momentum

-

The composite PMI is also slowing, underscoring broader moderation

Japan’s services sector continued to expand in March, although momentum showed early signs of slowing as rising cost pressures and geopolitical uncertainty weighed on sentiment.

Japan’s S&P Global services PMI fell to 53.4 from February’s 21-month high of 53.8, indicating a slower but still strong pace of growth. Activity has now increased for twelve consecutive months, supported by stable demand and improving client numbers, with finance and insurance making gains in the sub-sectors.

However, the underlying tone of the report pointed to moderation in future momentum. Growth in new orders slowed to a three-month low, with companies reporting only modest increases in business volumes. While domestic demand has remained resilient, the pace of expansion has slowed compared to previous high levels. Export orders also rose, but at a moderate rate despite being one of the stronger readings in recent months.

At the same time, cost pressures have intensified significantly. Companies recorded the largest rise in input prices in nearly a year, with participants widely citing rising costs of energy, fuel and raw materials. The escalation of conflict in the Middle East has been particularly highlighted as a key driver of these price increases, enhancing the transmission of global energy shocks into domestic inflation dynamics.

Although companies continue to pass on higher costs, the pace of output price inflation has eased slightly from a multi-year peak in February, suggesting some limits to pricing power.

Labor market conditions also showed signs of caution. Employment continued to rise, but at a slower pace, while backlogs eased, indicating reduced pressure on capacity.

Notably, business confidence deteriorated sharply, falling to its lowest level since the pandemic. Companies pointed to growing uncertainty linked to the conflict in the Middle East and its effects on global demand and inflation, highlighting a more fragile outlook despite the continued expansion.