Listen to the audio version of this article (generated by artificial intelligence).

Tom Young is here with your Sunday digest.

In the days following the IPO Space Exploration Technologies Company (Spex) Its shares rose 25%, rewarding early investors and turning its owner, Elon Musk, into a trillionaire. The following week, the stock price fell below $160, turning most investors off and forcing Musk back into the “modest” hundreds of billionaire category.

SpaceX is not alone in its ups and downs. In the same week, shares Micron Technology Company (in) It fell 15% on a broader technology sell-off before straightening back up on massive gains.

As a Senior Analyst at InvestorPlace Louis Navellier noticed recently Market 360 problem, The AI market has been all over the place lately.

Now, this sometimes happens during late rallies. Traders know that some stocks are overbought, so they sell them at the first sign of trouble. A small drop can lead to panic.

But as I mentioned in Last Sunday digestThis volatility is also a byproduct of artificial intelligence. Millions of trading algorithms, advisors, and investors increasingly rely on the same AI-powered tools. It creates a new type of “trading convergence” that gets people in and out of stocks at the same time.

This can lead to huge losses of wealth when trades go wrong.

That’s why Lewis rarely haunts the audience. Instead, it looks for signs that commonly occur before AI systems catch the wind with the help of their eponymous system Precursor Intelligence (PI). It helps him find companies that improve fundamentals and accelerate money flow before Every AI tool is jumping on board. You can click here to hear him talk more about it.

Last week I featured three of these top picks: Texas Instruments Inc. (Texan), Harmonious Energy Systems Company (MPWR)and Oncology Institute (TOI).

This week, I’d like to add two more.

Stocks to buy #1: The dark horse of artificial intelligence

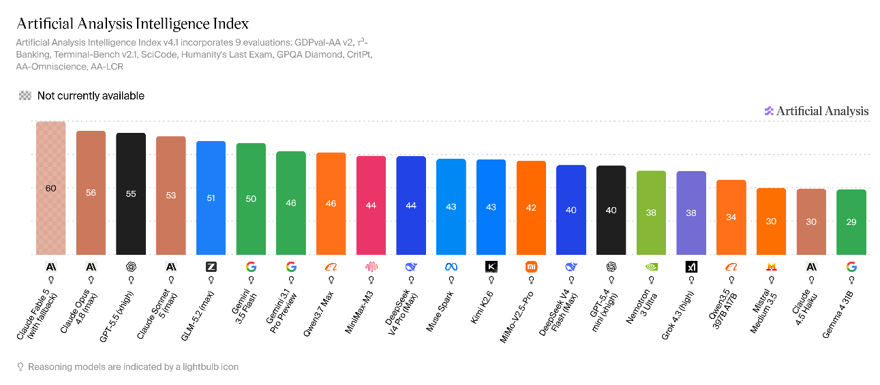

Over the past two months, shares have risen Alphabet Company (Google) It has lagged behind the broader AI market. The top-rated Gemini model is now the fifth best, as ranked by Artificial Analysis, an artificial intelligence measurement company. It will soon drop to sixth place when testing of the latest version of GPT-5.6 from OpenAI is finished. Alphabet shares have fallen 10% since their peak in mid-May.

Gemini (dark green) is starting to look pretty average

However, the Lewis System believes that this downward trend is exaggerated. The company gets an “A” in its “Follow Money” grade and has the receipts to back it up. The company is one of the fastest-growing companies in our equity universe, and is the only hyperscale AI data center company whose cash flows are expected to remain positive in every quarter this year.

I think this assessment is correct in many respects I explained last month. Alphabet has a dominant search business, powerful data center chips, and momentum against OpenAI. Together, this suggests that its fair share value is somewhere in the mid-$400 range; It is now trading at around $355.

The recent launch of an artificial intelligence model by Chinese startup Z.ai reinforces this conviction.

On June 13, Z.ai launched a large language model (LLM) called GLM-5.2, which synthetic analysis determined to be better Of the two main models of Alphabet. And after testing the new LLM, I think this is a surprisingly good development for Alphabet because the system is Completely open source. Users can download GLM-5.2 for free, read its source code, and take anything they want for their own use.

In other words, Alphabet could take the model for itself.

This should be a windfall for the search giant, which was previously fighting two separate battles:

- Low-cost single-user models for Google Search, Android, and

- Sophisticated models for attracting enterprise users to Google Cloud Platform.

The GLM-5.2 helps combat this first, since it’s good enough for everyday use and surprisingly cheap to run. You don’t need a sophisticated model to give directions to the nearest golf course… and you certainly don’t need a model to set your phone alarm for 7 a.m. All you need is something reliable enough not to wake you up at 3 a.m. or send you to the wrong place.

This means Google can focus on this second area, where it already performs well. The company doubled the number of deals, which ranged between $100 million and $1 billion, in the last quarter. Now that it can focus its efforts on cutting-edge AI models, it is likely to continue to stay ahead of its competitors in the coming quarters.

Thus, I still see more upside in Alphabet. Shares are already up 27%. Since I tagged them last November (Even with the recent withdrawal), they still have more room to climb.

Stocks to buy #2: The resurgence of US drug development

Last week, I wrote about the US government I was suddenly pro-pharma again.

In April, Health and Human Services (Department of Health and Human ServicesSecretary of State Robert F. Kennedy Jr. told Congress that “China is now eating our lunch” in drug development and promised to make changes.

Since then, the agencies RFK Jr. oversees have changed almost 180 degrees. In June, one group unanimously recommended the first vaccine to the current administration, and a separate group launched a project called Operation TrialBlazer to accelerate clinical research.

I recommended Oncology Institute Inc. (TOI) as a stock to buy.

This week I’d like to add another healthcare company to this list:

Moderna Company (mRNA).

Moderna is probably best known for its development of the Covid-19 vaccine, a treatment that took just 10 weeks to develop and another 10 months to reach approval. You may also know that Moderna’s stock price fell more than 94% between 2021 and 2025 after demand for vaccines declined and mRNA vaccines became a lightning rod for the culture war.

It wasn’t easy for the drugmaker. In President Trump’s first year back in office, the Department of Health and Human Services terminated Moderna’s contract for the avian influenza pandemic, stopped recommending COVID-19 vaccines for healthy children, cut $500 million in mRNA vaccine funding, and removed all 17 members of the Centers for Disease Control and Prevention (Center for Disease Control) Vaccine Advisory Committee. Moderna was forced to cut back projects and direct its remaining funds to a smaller number of higher-priority clinical trials.

But it looks like the drugmaker is back. On June 18, FDA advisors backed Moderna’s mRNA flu vaccine, leading to a 20% rally in the stock. At about the same time, MRNA moved from a “C” grade in the Lewis system to a “B” grade in extraordinarily high smart money buying.

The basic story has improved since then. On June 25, the company provided exciting details at its annual Science Day, indicating much faster growth for its oncology drugs, known as “cancer vaccines.” These are programmable treatments that can be tailored to individuals or target common cancer markers more broadly for off-the-shelf use.

Moderna’s most promising tailored drug, known as intismeran autogene, is currently undergoing phase III trials for the treatment of melanoma. The results will be published by the end of this year, and analysts expect annual revenues of more than $3.5 billion by 2035. The same treatment is also being tested on kidney cancers, lung cancer and other diseases.

The company is also working on several off-the-shelf treatments that are showing early promise. At least one of these treatments should be a hit, according to analysts at Morningstar, and could lay the foundation for “multiplex” treatments. This is where a single drug seeks multiple targets at once, increasing the likelihood of success.

More importantly, Washington’s mood toward drug development is changing. Robert Kennedy Jr. himself said that China “went from doing 3% of clinical trials to doing 30%,” and that “we are losing scientists, we are losing our intellectual property… and we are going to lose our biosecurity.”

If the federal government wants to flood the region with money to develop more drugs, Moderna is the most obvious candidate. Development of programmable mRNA vaccines is incredibly fast, and this pharmaceutical company has a lot of partial development ready to resume.

Walk away from the crowd

You’ll notice that Alphabet and Moderna aren’t the most popular names among retail investors. Google is often seen as too big to grow further, while the politicization of vaccines has turned a generation of investors away from Moderna altogether.

Here’s why this matters: AI systems are exceptional at pricing what’s already in the numbers. They can “see” everything that has happened over the past five decades, and often know exactly what investors are doing today. They are also relatively good at extrapolating whether the future is similar to the past.

What artificial intelligence does no Do it well is to predict changes. The reality is that Alphabet and Moderna both run platforms that can adapt quickly. Alphabet could take a free, open source model like GLM-5.2 and turn it into dozens of cheap consumer products overnight. Moderna’s programmable mRNA makes it possible to direct the same basic technology to everything from influenza to skin cancer.

This is the real opportunity in a market governed by trading convergence. The more investors rely on the same tools that only see today’s data, the less they will price companies whose best chapters have yet to be written.

This is exactly what Lewis built Precursor Intelligence to do. He looks to identify companies with strong fundamentals and accelerating cash flow.

Lewis just recorded a presentation walking investors through this system, and how it predicts a big rally in stocks outside of AI. So, if you want to get ahead of the next wave rather than get swept up in it, I urge you to: Watch Lewis’s free stream here.

All of us here at InvestorPlace wish you a Happy 4th of July.

Until next week,

Thomas Young, CFA

market analyst, Investor location