The price of gold (XAU/USD) is trading near $4,676 on April 3, up nearly 17% since hitting a low of $4,105 on March 23. The assembly looks convincing. However, the private correlation measure, options position change, and a close reading of the latest Trader Commitment report suggest that the current progress may be based on a false foundation.

Gold’s strongest rallies historically began after the metal separated from oil, rather than while they moved up together. The 17% retracement sees the same trading that preceded every correction in this cycle, and a controlled decline that breaks this correlation could be more positive than further upside.

Gold is rising but the important correlation is already starting to change

Since March 23 The price of gold has increased iThere is an ascending channel on the 8-hour chart. The structure is not a bear flag, as the channel has extended beyond the typical duration, but its bullishness is also not confirmed until the upper boundary is broken decisively.

The XAU-WTI Correlation Matrix, BeInCrypto’s custom indicator that measures the 50-period rolling correlation between spot gold (OANDA:XAUUSD) and WTI crude oil (TVC:USOIL), currently reads -0.10. The reading has retreated from the positive territory it occupied in March, but it appears that it has begun to rise again.

The pattern is consistent. In mid-October, the correlation dropped to around -0.88. It remained negative until early November. That was when the gold price launched its strongest rally. This shows that gold performs best when it is completely separated from oil, acting as an independent safe haven.

Every time the correlation peaks in positive territory, gold corrects. In late January, the reading was around 0.85, and gold fell over the following weeks. In early March, there was another positive peak in line with the $5,422 high before the sell-off resumed.

The current reading of -0.10 puts the correlation in transition. The 17% rebound since March 23 occurred during this transition phase, meaning it was partly driven by the same oil-related sentiment rather than independent safe-haven demand.

For this reason, a controlled decline will be constructive. If the price of gold declines while oil continues to rise, the correlation will accelerate towards the -0.70 region, exactly where Gold was released Each independent pool is sustainable this cycle.

The rally does not need to continue gold’s uptrend. The link needs to terminate reset. Options traders have already begun to react to the bounce, and their positions reveal whether the current move has real conviction.

Bullish bets have replaced bearish bets but the basis is reaction

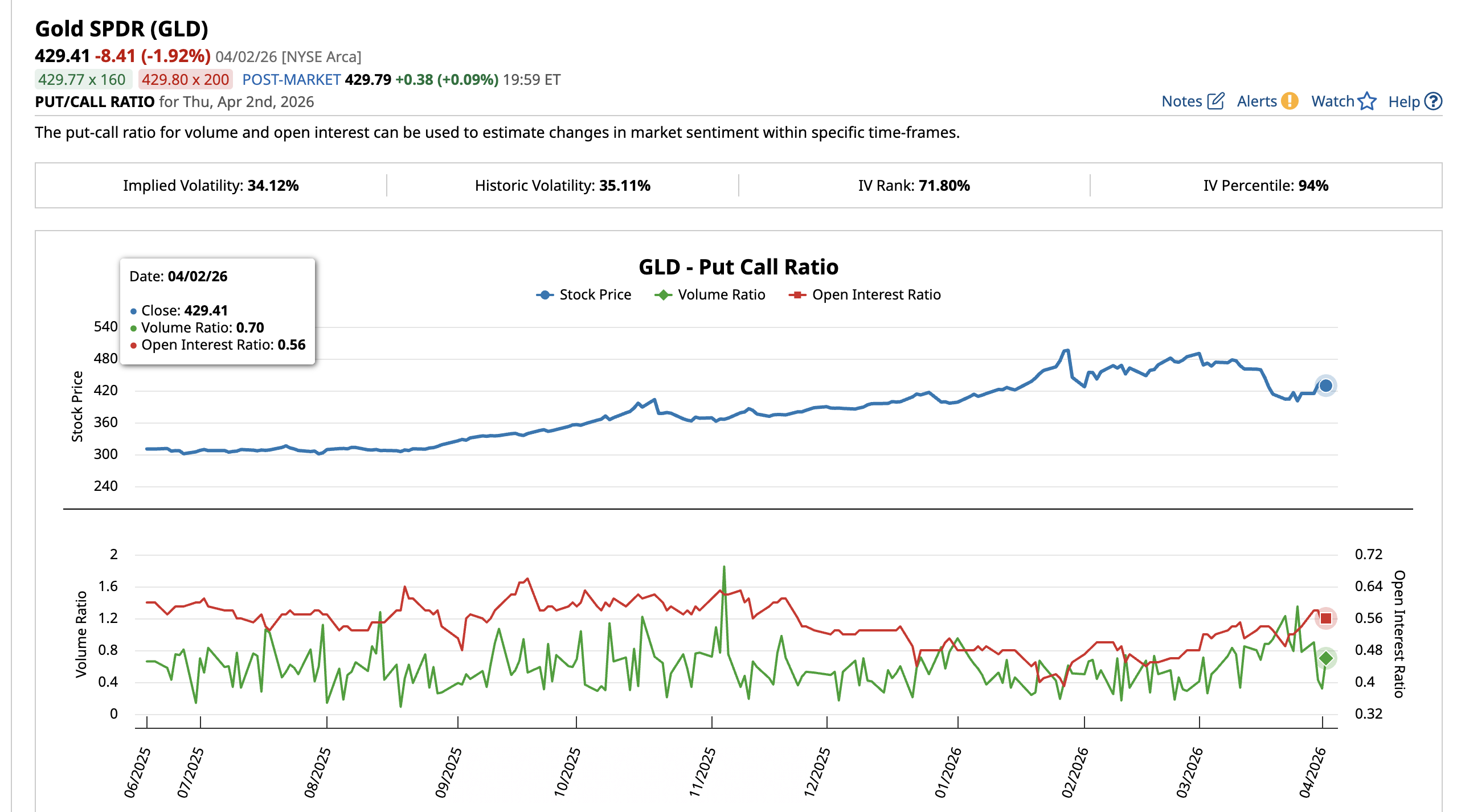

The put ratio in the SPDR Gold Shares ETF (GLD) shows how options traders position themselves around the price of gold. On March 26, the put volume ratio was 1.35, meaning that a much larger number of calls were traded than were traded. Bearish sentiment took over. The open interest ratio at that time was 0.53.

By April 2nd, the volume ratio had collapsed to 0.70 as call activity picked up and volume faded. The open interest ratio rose to 0.56, indicating that new long positions were opened. The bearish bets that dominated during the March sell-off have been replaced with new bullish exposure.

Traders likely responded to the 17% bounce by shifting from protective buys to trend calls. When bullish bets accumulate at the same time as the oil correlation rises (current state), newly opened long positions become vulnerable.

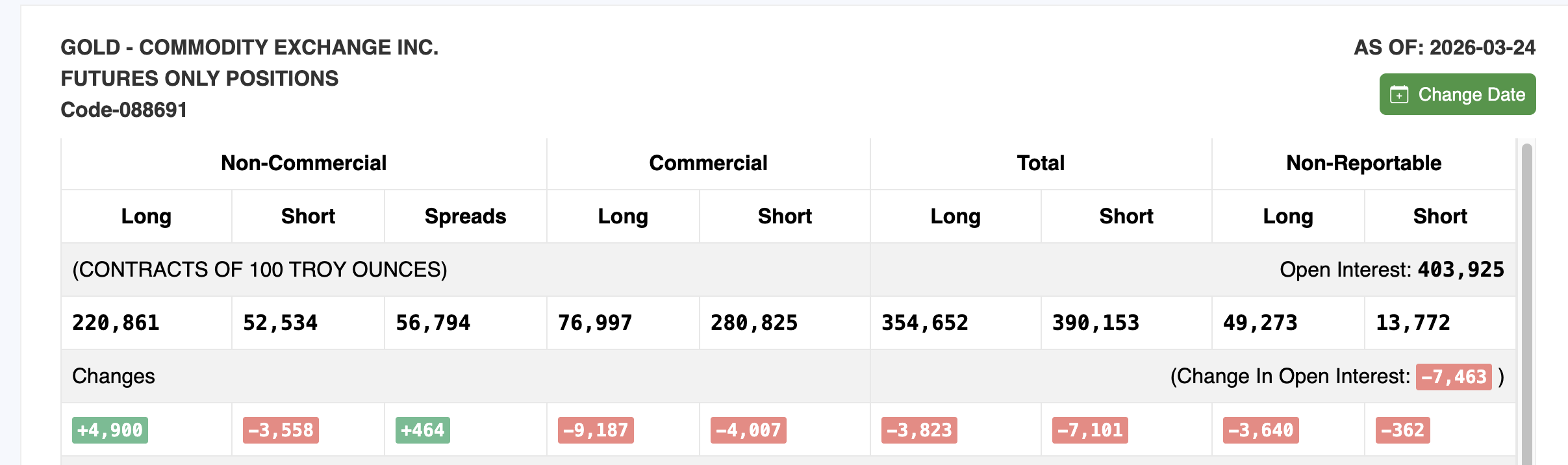

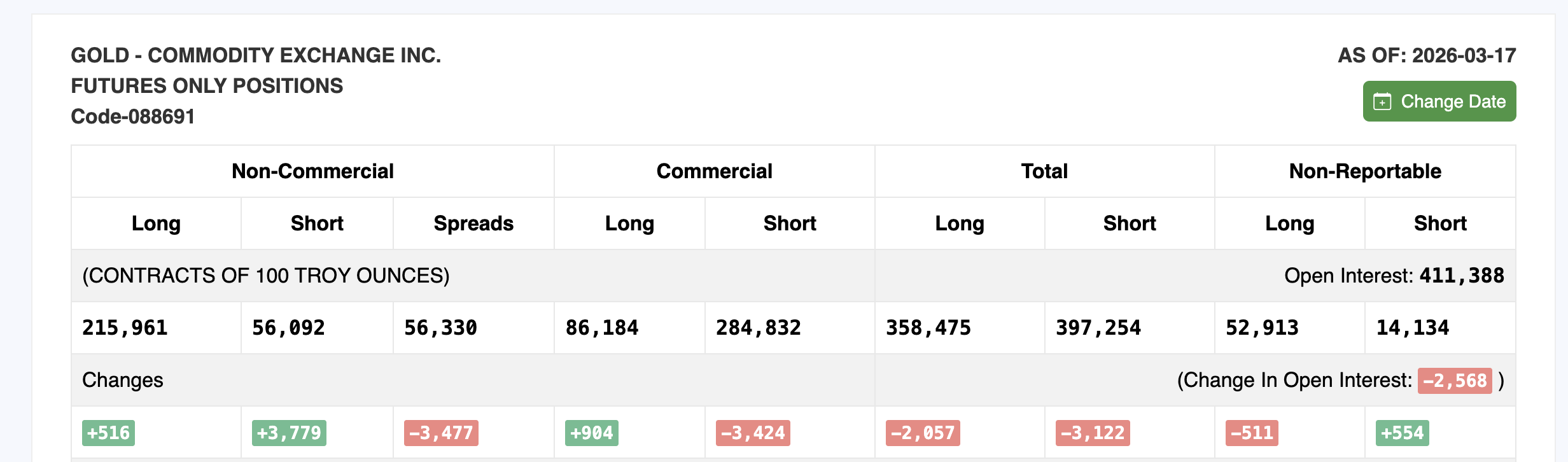

The Commitment of Traders (COT) report, published weekly by the Commodity Futures Trading Commission (CFTC), reinforces this reading. The March 24 report, the latest available, shows that non-commercial (speculative) long positions increased by 4,900 contracts to 220,861. Short positions decreased by 3,558 to 52,534. On the surface, this looks bullish.

However, total open contracts decreased by 7,463 contracts to 403,925 compared to the previous March 17 report. When long positions increase but total open interest decreases, this usually means that the rise is driven by short covering rather than new buying conviction.

The shift between the two reports is consistent with what GLD’s call data shows. Bearish participants were caught by the 17% rally and were quick to reposition their positions. This dynamic can sustain movement temporarily but historically does not provide the basis for a lasting advance in the gold price. Price levels now determine the next path for gold.

The price of gold and the paradox of correlation

8-hour chart with Fibonacci levels surrounding each critical level of gold price. Gold is currently at $4,676 inside the ascending channel.

For the rally to continue, gold needs an 8-hour close above $4,802. Above that, $5,043 acts as the next major resistance level. A move through $5,043 will refocus on $5,422, the March 1 high.

However, if Gold reaches $5,043 or higher before the correlation completes its reset into deep negative territory, the rally risks repeating the same pattern that preceded both previous corrections. A move higher while the correlation remains near neutral rather than resetting below -0.70 would leave the advance on an incomplete basis.

On the downside, the first support level is at the 0.236 Fib level of $4,490. Below that, $4,297 comes into play at the 0.382 Fibonacci level and $4,141 at the 0.5 level. The $4,105 low as of March 23 closely matches the 0.5 area and represents the base of the 17% rally.

Here the paradox is resolved. A decline in the price of gold towards US$4,105 while oil continues to rise could push the correlation back into negative territory.

A decline that breaks the oil correlation creates a stronger foundation for the next sustained move, while a sustained rally that keeps both assets moving together leaves gold in the same overheated zone that has led to every correction in this cycle. An 8-hour close above $4802 extends the channel rally but keeps correlation risks alive, while a pullback towards $4105 that breaks the oil link could paradoxically be the most bullish outcome for gold’s medium-term path.

this post Why could gold’s price decline be more bullish than its current 17% rise? appeared first on BeInCrypto.