Listen to the audio version of this article (generated by artificial intelligence).

May’s CPI was hot — but we dodged a bullet… The labor market’s handbrake is on… What a rally means for AI stocks… An edge to a diverging stock market

The May Consumer Price Index (CPI) report was released this morning, and the initial reading was as good as investors could have hoped under the circumstances.

The headline inflation rate was 4.2% year-on-year, which was in line with expectations. Yes, this is the highest reading since April 2023, and yes, it crossed the 4% threshold for the first time in three years. But the monthly pace actually Slow down – 0.5% in May compared to 0.6% in April.

Meanwhile, the Fed’s most important figure — the core CPI, which excludes volatile food and energy — came in at just 0.2% on the month, below expectations of 0.3% and April’s 0.4% reading.

Gasoline made up the bulk of the main monthly movement, while shelter, food and basic goods costs were well-disposed. Economists are increasingly calling May the peak month – assuming that hostilities with Iran do not reignite and push oil prices higher again.

The bottom line: So far, this is an energy-driven inflation boom, not a broad-based one – which makes it a relatively good news moment in a difficult period of inflation. If core inflation had reached high levels, it would have shaken an already fragile market. So, the bullet dodged.

However, the print of the CPI tells us where we were. What’s changed beneath the surface tells us where we’re going—and what’s changed is already important enough that even a well-disposed basic reading doesn’t change course.

In other words, the risk of inflation has not disappeared. The fragile balance that had prevented the Fed from responding to it began to crack.

The handbrake is released

For the better part of six months, the Fed has been frozen between two competing fires.

On the one hand: the inflation rate is much higher than the 2% target…

The Iranian conflict has added to the energy shock, pushing the headline CPI to 4.2% – the highest level in three years, as of this morning’s edition. Lowering rates in that environment means adding fuel to the fire.

On the other hand: the labor market is showing real signs of weakness.

He spent most of 2025 in decline – slow hiring, declining job creation, and unemployment drifting toward 4.5% at its peak last November. It wasn’t in free fall, but it was fragile enough that walking in it presented real risks.

But this weakness in the hands creates a delicate balance. Inflation had driven interest rates so high that it was not possible to lower interest rates, yet the labor market was too fragile to raise interest rates.

The result has been paralysis: Interest rates have held at 3.50% to 3.75% for three straight meetings, which is good for Wall Street.

But that calculus may now be changing – and the evidence is coming from an unexpected place.

One of the strongest arguments for labor market fragility has been the fear that artificial intelligence is quietly hollowing out the hiring process. If true, it would give the Fed more reason to stay put. But the data tells a different story.

As normal digest Readers know I’ve been wondering about the “AI will take over all jobs” narrative. I haven’t given up on it, but the increasing amount of data makes me cling to it with less conviction.

Yesterday, Torsten Slok, chief economist at Apollo Global Management, pointed out the latest relevant data point.

Rather than AI-related job losses increasing, Slok reported that the number of job openings per unemployed worker has started to rise again and is now back above 1.0 – meaning there are more jobs available than workers to fill them. Last Friday’s May jobs report reinforced this, as non-farm payrolls jumped by 172,000 jobs.

Here is Ghalib:

If artificial intelligence were sparking a job crisis, we would expect job opportunities to collapse and unemployment rates to rise, but the opposite is happening.

Source: Torsten Slok/Apollo

This is big.

The labor market weakness that gave the Fed the excuse to stay put is fading. Which means removing one of the two constraints that support the Fed’s delicate balance.

What does Warsh’s first meeting mean?

Kevin Warsh was sworn in as the Fed’s 17th chairman on May 22, inheriting a central bank that has held interest rates at 3.50% to 3.75%, a closely divided Federal Open Market Committee — four dissented at the last meeting — and inflation that has been above the 2% target for five straight years.

Three of these four dissidents were not opposed to stopping. They were opposed to the Fed’s accommodative bias – language that suggests cuts, not rate hikes, is the next step.

Why do we lean toward easing when inflation has been hot for so long?

At the June FOMC meeting — a week from today — Warsh is widely expected to abandon this dovish bias entirely.

Now, that alone would be a meaningful hardline signal. But the deeper question, with the labor market brakes on, is whether the shift in bias is enough – or whether the data are supportive of a clear signal toward higher interest rates.

Markets are starting to price in this possibility.

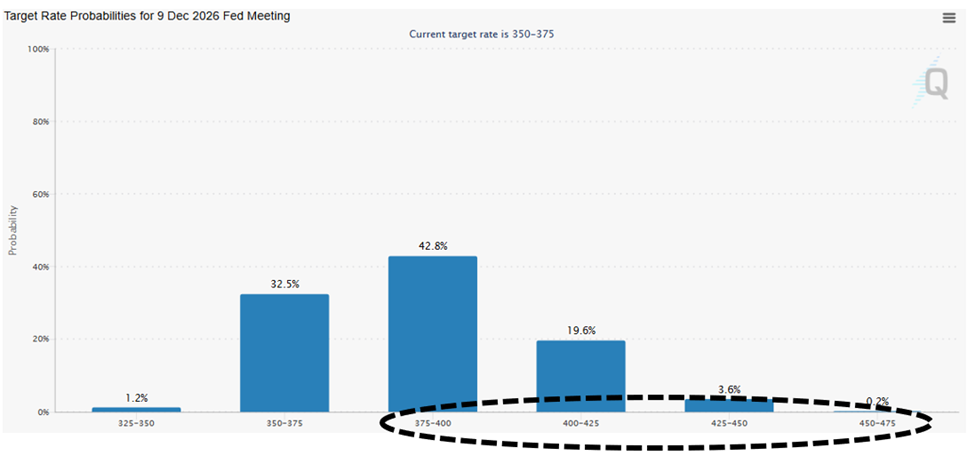

Below, we take a look at CME Group’s FedWatch tool, which shows the likelihood that traders will set different interest rate ranges in the future.

As you can see, the odds of a rate hike of at least one quarter point by the FOMC meeting in December 2026 are now about 66%.

In other words, the question now is not “When do we cut back?” But rather, “When do we hike – and how much?”

Two markets within one – and where AI trading fits in

Let’s assume that sometime in the coming months, Warsh takes a walk.

What happens next?

First, there is a massive sell-off. This is almost certain depending on how the markets behave.

High multiple Growth stocks They are nailed because higher rates mean higher discount rates, which pressures valuations on companies whose earnings are weighted toward the future.

So, AI darlings like nvidia (NVDA), arm (arm), and marvel (MRVL) They all suffer in the immediate aftermath of the price hike announcement.

But as wise investors, we have to look beyond that. After all, the first step is permanent Moving is completely different issues.

While a knee-jerk sell-off will treat all interest rate sensitive assets in much the same way, a recovery will not happen.

To understand the difference, we must ask one key question…

What is fueling today’s AI bull?

Answer: super scale. Microsoft (MSFT), alphabet (Google), Amazon (Amzn), and dead (dead).

But while these companies use some debt to build out their AI capex, the majority of that financing comes from operating cash flow and issuing new equity, totaling tens of billions of dollars per quarter.

Raising interest rates by 25 or 50 basis points does not change this calculation. These companies don’t need cheap debt to build data centers. Their spending on AI infrastructure is, to a large extent, insulated from the Fed in a way that most markets are not.

Contrast that with what a real tightening cycle would do to the rest of the market: high-capitalization properties, small-capitalization companies operating with thin lines of credit, and discretionary consumer names relying on households that borrowed cheaply…

This pain is structural, not temporary, and it does not bounce back in the same way.

This will accelerate the “Tale of Two Markets”

normal digest Readers will recognize this dynamic. It’s the “technology” we’ve been writing about for years at this point — the widening gap between companies and investors positioned on the right side of transformative technology, and everyone else.

What is worth understanding now is that the high-rate environment does not stop the technical phenomenon, but rather is likely to accelerate it.

If monetary tightening hits interest rate sensitive sectors hard while leaving highly expansive AI capex largely intact, the performance gap between AI infrastructure and the rest of the market widens.

This is a harder story to tell than “interest rates rise, growth stocks fall.” But it’s the most subtle—and it’s the distinction that matters in how you think about positioning.

And this is exactly where legendary investor Louis Navellier comes in

Lewis has spent 47 years fundamentally identifying the strongest stocks in the market. But in a bifurcated market — where right names are recovering and bad ones are disappearing — finding quality is only half the equation.

The other half is timing: knowing when a stock’s short-term momentum supports action on a long-term thesis, and when it doesn’t.

This morning, Lewis and TradeSmith CEO Keith Kaplan held a meeting Live event unveiling a new system that combines Louis’ fundamental stock selection framework with TradeSmith’s market timing technology. The goal is precisely the type of feature that this environment requires, and not only What To own through a volatile and price-sensitive extension, however when To pull the trigger or step aside.

If you missed this morning’s event, You can catch a free replay here.

Coming full circle

Today’s Consumer Price Index (CPI) reading was relatively good news. but TRUE The news is how the handbrake is being released now.

A week from today, Warsh chairs his first FOMC meeting with inflation at a three-year high, the labor market no longer fragile enough to justify inaction, and markets estimating a 66% chance of a rate hike before the end of the year.

The system is changing, and the technology gap will widen.

The investors who step up are the ones who understand what this means, where it leads us, and how to prepare for it.

I wish you a good evening,

Jeff Remsburg

(Disclaimer: I own MSFT, GOOGL and AMZN)