This is part of the 0xResearch newsletter. To read the full editions, Subscribe.

While cryptocurrency prices have shown a modest recovery in the short term, the negative breadth and relatively weak performance of TradFi benchmarks on a monthly basis indicates a prevailing bearish environment.

Zooming out, we look at secular growth trends within stablecoins and lending as solid sectors for multi-year growth.

Indicators

Cryptocurrency markets remain range bound after November’s brutal sell-off. Last week showed a modest recovery, with Bitcoin reaching $90,400, now 12% below its recent corrective low of $80,700. Over the past 24 hours, the AI and Modular sectors have been the biggest winners, with TAO (+6.4%) and TIA (+6.2%) being notable contributors to this short-term strength. The Perp index was the biggest loser, with DYDX (-3.1%) and HYPE (-0.6%) contributing to the sector’s weakness.

Looking at the monthly picture, the picture remains unfavorable. TradFi indices like Gold, Nasdaq, and S&P 500 have all been in the green over the past month, while every cryptocurrency index we track is measuring negative returns.

Breadth is decisively negative on a monthly basis for all cryptocurrency indices, with no safe haven provided. It is worth noting that the Protocol Revenue Index is the best performing among cryptocurrency sectors, indicating relative strength in protocols with strong fundamental positions.

Despite the recent strength, it remains to be determined whether this rise is a countertrend to a longer-term downtrend, or whether the bottom will continue for the rest of 2025.

Market update

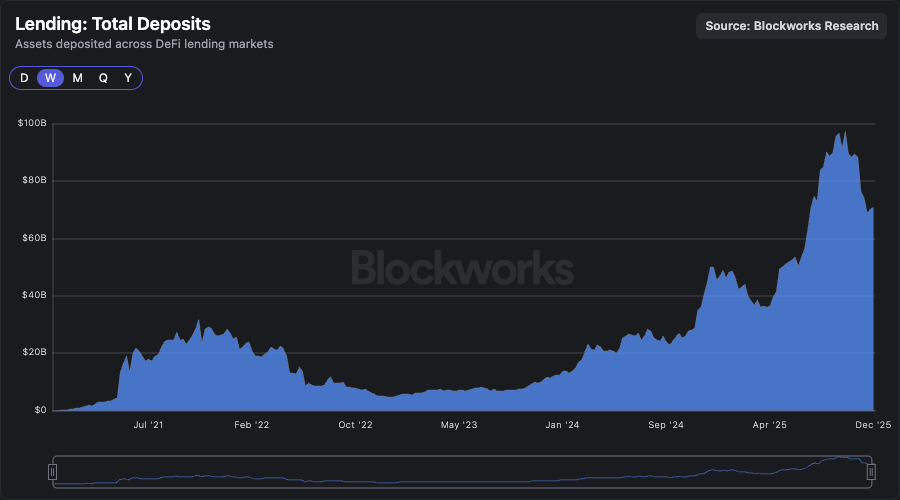

In the midst of a downtrend, don’t lose sight of the bigger picture, and take a moment to appreciate how far we’ve come. At the lows of the bear market, lending requests within DeFi accounted for just $5 billion in deposits, a rounding error within the larger financial system. In the years that followed, this number rose to $71 billion in deposits, after previously reaching nearly $100 billion.

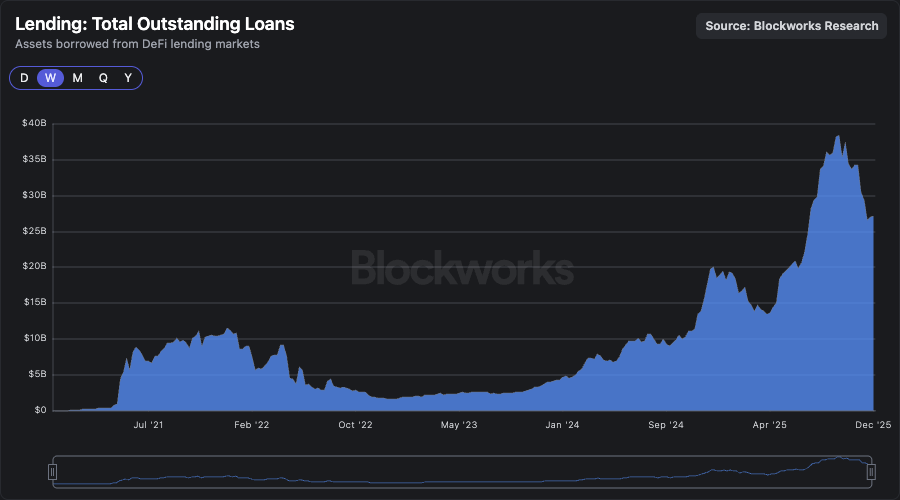

Likewise, outstanding loans on these orders were $1.6 billion at bear market lows. Since then, active loans have risen to over $27 billion now, and recently topped $38 billion. These numbers have grown to a scale worth paying attention to, and not just for native crypto users. Divergence can cut both ways, to the upside and to the downside, for both key metrics and spot prices. But 20-fold growth in key metrics in just a few years indicates that this sector is still far from its ultimate growth rate.

Amid the decline in cryptocurrency prices, the total supply of stablecoins returned to an all-time high of $310 billion, after a brief period of -$10 billion in outflows.

Growth in stablecoins is a trend I wouldn’t bet on. Onchain financial markets stand as a major beneficiary of the growing supply of stablecoins, which they claim are their primary applications for use. Stablecoin lenders seek yield, while borrowers seek leverage. While spot assets will remain volatile, this secular trend should remain an ongoing and solid tailwind for DeFi applications.

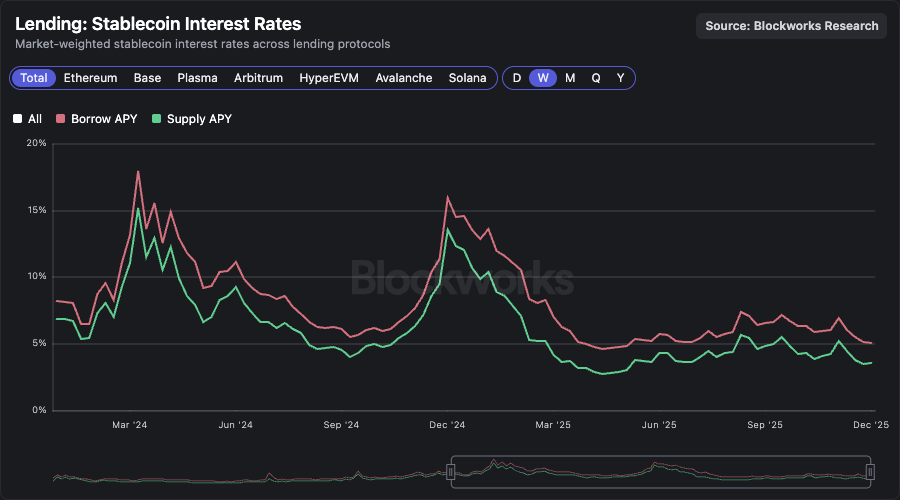

It is worth noting that the continued growth in the supply of stablecoins comes amid very modest on-chain returns. Standard lending application bid rates are 3.6%, which is lower than the SOFR of 3.9%. The increasing depth in onchain stablecoin liquidity may continue to dampen the upside in supply rates, and in the absence of a material risk premium for legacy rates, growth in the use of stablecoins in financial markets may falter.

Get news in your inbox. Explore Blockworks newsletters: