Why is the public reading the data wrong – and what would Louis Navellier predict instead?

Listen to the audio version of this article (generated by artificial intelligence).

From two downgrades to a rise in five months… Why Lewis says the market is misreading this… The Besant-Warsch playbook… How to position yourself before the pivot… How to catch a repeat of yesterday’s event with Lewis

At the start of the year, CME Group’s FedWatch tool showed traders pricing in two interest rate cuts for the year, with the first expected as early as April.

As I write Thursday morning, the forecast has changed…

The FedWatch tool now shows a probability of about 34% for the rate to lift.

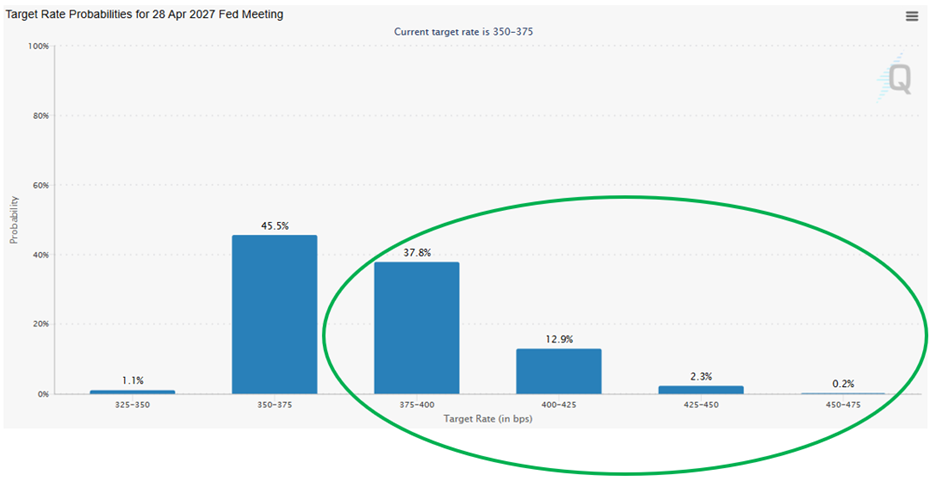

These are just December forecasts. If we look to April 2027, the odds of raising interest rates will rise to approximately 53%.

Source: CME Group

This is a stunning swing in market expectations in just five months. It raises an obvious question for investors…

Is the market right?

Legendary investor Louis Navellier, editor Stock breakoutI don’t think so.

I’ll get to Lewis’s argument in a moment. It has direct implications on how you are now.

But first, let’s make sure we’re looking at the same chessboard.

How we got here

As a quick recap, the CPI on Tuesday reached 3.8% year over year – its highest level in three years. The producer price index — the wholesale inflation reading — fell 6.0% on Wednesday, the biggest 12-month jump since December 2022.

In the wake of this hot data, expectations of interest rate cuts not only faded, but collapsed. An interest rate hike has become the expected next step in the market.

This makes sense. Hot inflation data means the Fed can’t cut interest rates. The longer the data stays hot – and it will likely get hotter – the more plausible the question becomes…

Is upside the most likely next step?

The futures market now responds “yes.”

But here’s Lewis’ opinion from yesterday Stock breakout Flash alert:

We should just take a step back and realize that we had 20% earnings growth with the S&P this quarter. Profits are expected to be good during the remainder of the year.

Stocks are a great hedge against inflation.

So, despite this market-shaking inflation news – CPI (Tuesday) and especially PPI (yesterday) – we are in a very good environment.

This is not a denial of hot prints. As I will explain, it is just an inference based on a different reading of the same data and headlines.

Why does Lewis think the market is misreading the inflation picture?

Those betting on higher interest rates are treating this week’s inflation rates as evidence of a structural problem.

Lewis treats it as evidence of a temporary shock layered on top of a more controllable fundamental trend – a crucial distinction.

Let’s start with Lewis on where inflation comes from:

We had this inflationary bubble of energy. We also have higher trucking costs and shipping costs due to higher costs of diesel, jet fuel, etc.

This will extend to all costs of goods and services, and this appears to be what was shown in the PPI (yesterday).

This is an important point that talk about raising interest rates ignores…

Printing a 6% PPI is not a story about rising wages or rising demand for consumer goods. It’s a story about the oil shock caused by the Iranian conflict that flows through the supply chain — through diesel, jet fuel, trucking and shipping — and shows up in wholesale prices.

Energy-induced inflation is qualitatively different from the combined type. It has a ceiling – a potential subtlety that is not available in the inline variety. This solution, as Lewis noted yesterday, may be closer than the market thinks, in part because of the well capping problem Iran is facing.

Here’s Lewis:

(Iran) can’t really pump oil right now because the wells are backed up.

If they cap the wells, they won’t be able to restart them for months.

A spot has been spotted in the Persian Gulf. We hope they don’t pump oil into the water because again, if you cap the well, you won’t be able to get it back up and running for months.

So, hopefully they will come to their senses and make a deal.

In Lewis’s view, Iran has a great incentive to end this matter. The longer the conflict lasts, the greater, perhaps permanent, damage it will inflict on their oil infrastructure – the very assets on which their economy depends. This is a great motivation to find a slope behind the clatter of swords.

Now, Lewis is not completely ignoring the risk of inflation. He noted that the costs of wholesale services rose by 1.2%. As I mentioned yesterday digestOnce services inflation takes hold, it can get sticky.

Where Lewis deviates from the rate hike crowd isn’t in that risk — it’s in what it offsets. He argues that AI-led productivity gains represent a structural deflationary force that current data has not yet captured.

So the question is not whether services inflation is real. Rather, it’s a matter of whether the productivity story is big enough to address over time.

Lewis thinks so. The futures market, at the moment, does not.

The structural case for mobilizing price hikes is missing

Let’s bring policymakers and their expectations of what’s to come into the mix…

Back to Lewis:

Kevin Hassett, Chairman of the Council of Economic Advisers, explained on Sunday that we will achieve 6% GDP growth this year.

GDP growth comes from AI-led productivity gains, and is not inflationary. They come from record energy exports, which helps put downward pressure on the trade deficit that adds to GDP.

Our consumer is healthy. We realize there are higher prices at the pump, but the consumer is generally healthier.

Now, don’t miss this: The Fed’s job is to manage inflation without killing growth — and that’s a tightrope…

But if the growth we are seeing is driven, in large part, by artificial intelligence – real productivity, not borrowing from the future with cheap money – then raising interest rates to kill inflation threatens to destroy the very engine that does the deflationary work.

The Fed knows this, which is why a rate hike scenario may be more bark than bite. This is part of Lewis’s argument.

Therefore, while the timing of a rate cut is uncertain, the direction, he believes, is not. So, banking action on raising interest rates is a longshot.

Treasurer Scott Besent was making the same productivity argument

At the Semaphore World Economics Conference in April – where the Iranian conflict had already sent energy prices soaring – Besant was clear about what he was seeing:

If ever there was a “transition team,” it’s this one.

I don’t think this will become an integral part of inflation expectations.

He added that the Fed “will need to cut interest rates,” while acknowledging that waiting for more clarity is reasonable.

In the wake of this week’s hot print, it’s fair to think that Besant’s timeline may have changed, but not his destination.

On the other hand, Treasury Secretary and future Fed Chairman Kevin Warsh is playing by the same playbook.

Like Lewis, Warsh believes that AI is doing something that inflation data cannot yet see: making companies dramatically more efficient, putting downward pressure on prices over time. In a Wall Street Journal In an op-ed last fall, he wrote that AI represents a “major force for dampening inflation.”

Think of it as a slow counterweight to the energy shock. It does not appear in this month’s Consumer Price Index. But it’s constructive.

We have covered the complete framework of workshops in our website April 29 digest. In short, he intends to lower the federal funds rate while simultaneously shrinking the Fed’s $6.7 trillion balance sheet – a coordinated strategy designed to normalize policy without abandoning the direction of travel.

Overall, here’s Lewis’ take on what to expect and when:

Treasury Secretary Scott Besent will clearly be very busy, and incoming Fed Chairman Kevin Warsh will have to work with his colleagues at the FOMC before we can even think about cutting interest rates. But we may get some later in the year.

Now, while the timeline for cuts is uncertain, Lewis isn’t waiting for certainty to act…

What this means for your wallet

Lewis has seen this movie before. Four times, to be exact.

Every time the Fed begins a sustained cycle of interest rate cuts, the same rules of the game unfold. Smaller, domestically focused companies – more sensitive to borrowing costs and more likely to benefit from US economic growth – become the biggest winners.

It’s not instant, but it’s consistent.

Here’s Lewis highlighting some of the small business winners from previous editions:

- 1995 Fed Pivot: Cisco +2,062%. Rise +2,800%. America Online +2,900%.

- 2001 Interest Rate Cuts: Frontline +1,513%. Hansen Natural +1.125%.

- Interest rate cuts in 2008: Lithia Motors +475%. IPG Photonics +665%.

- Covid Sale 2020: MARA Holdings +1,800%. Moderna +1,200%.

Various stocks. Different sectors. Same dynamic every time.

Louis’s Stock Grader system has been working throughout this early phase of the cycle. You have been marked 53 stocks show the early signals he identified in each previous window – Strong fundamentals, building institutional buying pressure, and consistent top ratings in his eight-factor model.

He calls him Exclusion list: Companies too small for big Wall Street funds to touch, but not too small for you.

He went to live in his country yesterday The Fed shock event To find out his most convinced picks from that list — and offer a free stock recommendation for just showing up. If you missed it, Replay is available here.

Come full circle…

The market is now pricing higher. Lewis prepares for cuts.

One of them is reading the chessboard correctly.

History indicates that it was Louis.

I wish you a good evening,

Jeff Remsburg