Listen to the audio version of this article (generated by artificial intelligence).

Is FCX’s decline a buying opportunity?… Eric Fry’s ‘Builders vs. Developers’ Framework Explained… 12 App Stocks Jonathan Rose Warns About

Editor’s note:🔊 Prefer to listen? Press the play button above To hear today digest.

One of Eric Fry’s favorite ways to capitalize on the AI infrastructure boom is in the middle of a double-digit decline.

Is it time to buy the dip – or reevaluate your investment thesis?

Eric – Our global macro investing expert and magazine editor Speculators – He has defended copper as one of the most structurally urgent commodities. The reason is clear and straightforward: Every major theme reshaping the global economy — AI data centers, electrification, electric vehicles, expanding the power grid — runs through copper.

As just one example of relevant demand, take today’s hyperscale data centers…

It’s basically a copper and aluminum exoskeleton wrapped around silicone racks. Therefore, as the need for these facilities accelerates, the demand for copper is also increasing. S&P Global expects global copper demand to rise from about 28 million metric tons today to 42 million by 2040.

But supply is where things get complicated – and where today’s price action is difficult to read

There are two malfunctions occurring simultaneously.

First, the war in the Middle East is redirecting cargo ships away from the Strait of Hormuz, creating bottlenecks and delaying copper shipments. When supply temporarily shrinks, traders price scarcity quickly—resulting in higher spot premiums, especially in import-intensive regions.

Second, Eric writes that starting last Friday, China began restricting exports of sulfuric acid, a chemical necessary for copper extraction. This is likely to constrain production at the source before actual shortages are realized. Traders have priced in this risk.

The result this year has been a rise driven by two distinct factors – real demand growth and supply risk pressures. Eric suggests that investors play both angles:

Because the copper rally is driven by two distinct forces – real demand growth and supply risk pressures – the best approach is to invest in stocks that win in either scenario.

On the demand side, the winners are energy and raw materials companies that benefit from copper consumption at record rates through AI infrastructure, power grids, and industrial expansion.

On the supply side, the winners are copper mines, whose profit margins expand when prices rise faster than their production costs.

The arrow located at the intersection of the two is Freeport-McMoRan Corporation (FCX) – The largest publicly traded copper miner in the world.

Eric has been trading it for years. Back in 2020, he said Speculators Subscribers to call options on FCX, predicting a new “commodity super cycle” should send them higher.

He was right. By July 2021, these participants had closed their trades for a return of over 1,000%.

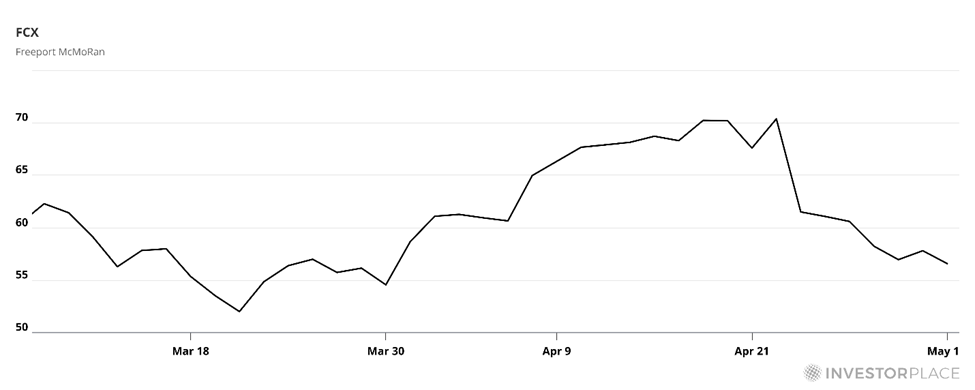

Which brings us back to the double-digit decline we mentioned at the top of the day digest – Hit FCX now.

Is this a buying opportunity?

Two weeks ago, the copper mining giant reached a new all-time high.

But a few days later, when Freeport announced its earnings, it cut its 2026 copper sales guidance from £3.4bn to £3.1bn due to operational setbacks at its Grasberg mine in Indonesia.

The market didn’t like it. Since its rally, FCX has fallen about 20%.

Is this a reason to be cautious about FCX? Or a good entry point for long-term investors?

Well, let’s start with the most important question…

Has the structural story that made FCX compelling changed?

No, we still have massive demand from building AI infrastructure, and the supply side can’t keep up – either way, FCX wins.

Here’s Eric:

When demand rises, FCX sells more copper in a strong market.

When a supply shock occurs, copper prices jump faster than FCX costs, expanding spreads in both cases.

Eric still had the FCX in his hand Fry investment report Portfolio with subscribers sitting on 247% returns.

This is a development that many investors today miss

The kind of booms that create tailwinds for commodities like copper don’t always reward companies that have spent billions on infrastructure as the big trend matures.

Indeed, this pattern of “builders don’t always win in the long run” has been repeated in almost every major technological transformation in modern history. As Eric says:

The builders struggled. Applicants became wealthy.

The reason is due to economics.

Builders face enormous upfront costs, constant reinvestment, and increased competition. As more capital flows in, returns compete. Compressing margins. Even if demand eventually arrives, it often comes too late for early investors.

in Friday digest SeizureEric reviewed the historical evidence (19th-century railroads, the construction of fiber Internet) and explained why he believes the same shift is starting to happen in AI today. It’s worth a read if you missed it, but here’s the short version…

Companies that have not built new technology infrastructure however user They were able to scale faster, operate more efficiently, and generate compounding returns compared to infrastructure builders who shouldered the massive capital burden of construction.

So, what is an example of an implementer poised to benefit today?

paypal (PYPL).

Eric says he’s deploying AI within the existing payments ecosystem rather than building infrastructure from scratch, and revenue per employee has risen more than 50% since 2022 as a result.

To dive deeper into the winners and losers of this shift, Eric has just released a new special podcast explaining the shift

It highlights how popular stocks may be at risk as the cycle unfolds, and details what lesser-known “applicators” can benefit from as the focus shifts from building technology… to making it work.

You can check it here. Eric even gives away his #1 Applied Stock to Buy today.

Now, to avoid confusion, FCX is not a builder in Eric’s framework – it is not pouring tens of billions into data centers and chips. Rather, it is the provision of raw materials that make the construction process possible.

Eric wrote that the real builders are the super-expanders: alphabet (Google), Amazon (Amzn), Meta Platforms Inc. (dead), Microsoft Corporation (MSFT).

These companies seem dominant today, and in many respects they are. But history suggests that as construction matures, more capital flows in, competition intensifies, and returns on infrastructure investment diminish.

So, keep timing in mind…

While builders often outperform in the early innings, the question Eric poses is who will win in the middle and later innings.

But not every “applicator” is the kind Eric recommends

This brings us to an important distinction — our trading expert Jonathan Rose, editor Masters in Commerce: Livehas been focused on.

Eric Apps are companies that use AI to create an existing competitive moat: a huge installed user base, proprietary data, or a dominant market position. Artificial Intelligence makes strong businesses stronger.

But Jonathan just pointed out a few companies he was pessimistic about that appear to belong to the same application category – but carry much greater risk.

We’re talking about software companies that are deploying AI, but using it to try to defend a declining model rather than expand a lasting one.

The moat was already eroding before the AI arrived. Today, AI is accelerating this erosion, and in some cases actively cannibalizing their revenues.

Jonathan presented his full case in Last Thursday for free Masters in Commerce: Live episode.

He flagged 12 names – with a combined market capitalization of $1.4 trillion – that he believes face significant downside risks over the next 24 months.

Jonathan’s framework focuses on four warning signs

They are called the “Four Stories”:

- Coordinated insider sales

- The defection of top talent to indigenous AI competitors

- Moving away from per-seat pricing towards consumption models

- And the CEO language that matches every previous disruption cycle – the “AI enhances, not replaces” playbook.

Although the software sector has already suffered a painful decline in recent months, Jonathan believes there is more to come:

Not disabled. It’s spinning.

We’ve seen this scenario before – Chegg, Teleperformance, Fiverr – and the pattern repeats itself.

I’ll give you three companies that are on Jonathan’s red flag radar. The first two are sales force (Customer relationship management) and Service Now (now).

Salesforce is the dominant CRM platform — the software that helps companies manage sales pipelines, customer data, and marketing campaigns. For years, this has been the gold standard for enterprise software.

Meanwhile, ServiceNow sells workflow automation software — systems that route IT help tickets, HR requests, and approval processes through large organizations. It has been one of the most beloved names in enterprise software for the better part of a decade

Jonathan sees both as a risk to your portfolio as AI continues to spread.

The third company is likely to raise some eyebrows…

that it palantir (Belter) – One of the highest-yielding stocks in the entire market over the past few years.

It has generated tremendous returns for investors who have ridden it and has become a well-known name in the retail investing community.

While its defenders will argue that it’s one of the rare software names that was actually designed for the age of artificial intelligence rather than threatening it, Jonathan sees something else:

CEO Alex Karp and four other senior executives presented same-day sales at the same reference price — $205 million in insider-coordinated intent.

The smart money inside is beating the record.

When the people closest to the company prepare to make a coordinated exit, Jonathan takes it seriously – regardless of the narrative.

So, how far can PLTR fall?

Jonathan’s model suggests that it may reach 45%.

PLTR reports earnings today after the bell – it may already be out by the time you read this. If Jonathan revises the numbers, we’ll update you here at digest.

But for now, you can hear more about his case against PLTR – and access the remaining nine names on his watchlist – at Last Thursday for free Masters in Commerce: LevThe webcast is here.

And to subscribe to Masters in Commerce: Live So you don’t miss any of Jonathan’s free market analysis and updates, Click here.

wrap

We have a simple line of communication today…

AI is reshaping where value is accumulated in the economy, and the winners are not always what the consensus predicts.

Copper sits upstream from construction. The real applicators sit downstream. And some of the most popular software names of the past decade may be stuck in the middle – with AI eroding the moats that made them great.

We will continue to track the three dynamics here at digest.

I wish you a good evening,

Jeff Remsburg