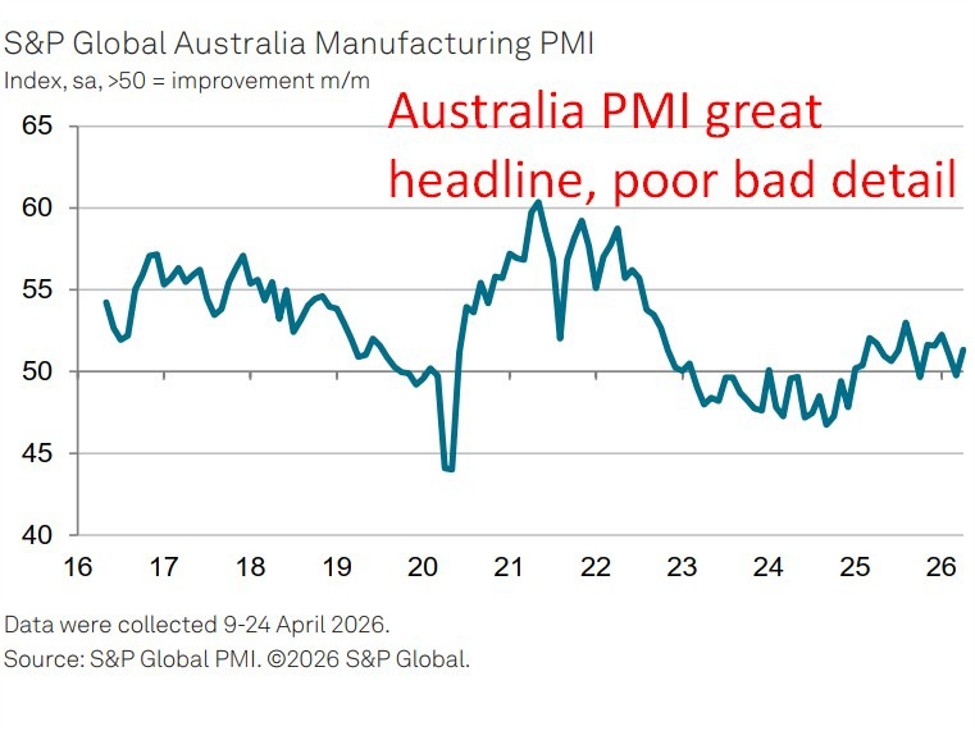

Australia’s April manufacturing PMI came in at 51.3 versus 49.8 in March, but the headlines were better. Input costs are the fastest in 4 years, and supply delays are the worst since July 2022. Output, new orders, and employment all declined. The aforementioned Middle East war.

summary:

- The S&P Global Australia Manufacturing PMI rose to 51.3 in April from 49.8 in March, back above the 50.0 flat mark, but the headline reading was driven by supply chain disruption and inventory building rather than a real improvement in demand.

- Supplier delivery times have been lengthened to the greatest degree since July 2022, and as longer delivery times are reflected in the Purchasing Managers’ Index (PMI) calculation, this has automatically inflated the headline indicator.

- Input cost inflation accelerated to its fastest pace in more than four years, with nearly 69% of survey respondents reporting a rise in input costs during the month; High fuel prices were identified as the main driver

- Output price inflation also rose, reaching the fastest rates in the decade-long history of the survey, indicating significant traffic pressures in the industrial supply chain.

- New orders continued to decline, with new export business falling for the first time in four months; Production fell for the third month in a row, and the latest decline was the fastest in 16 months

- Hiring was cut for the second month in a row as companies responded to lower order books by not replacing leavers and cutting working hours.

- Despite lower production requirements, manufacturers have increased purchasing activity and built input inventories for the first time in seven months, with anecdotal evidence suggesting safety stocks are being deliberately built up ahead of further expected price rises and supply delays.

- Business confidence fell for a third straight month to its lowest levels since July 2024, with conflict in the Middle East, associated inflation and cost of living pressures cited as major concerns.

- There is still some optimism remaining in the outlook for next year, with manufacturers expressing hope that the end of the conflict will improve demand and operating conditions.

Australia’s manufacturing sector posted a PMI reading above 50 in April for the first time since February, but the headline figure offers little real comfort. The index rose to 51.3 from 49.8 in March, but the improvement was almost entirely the result of supply chain disruptions and the build-up of defensive stocks rather than any recovery in underlying demand. Beyond these distortions, the picture is of a sector under constant and intense pressure from the conflict in the Middle East.

The mechanics of calculating the PMI mean that longer supplier delivery times, which are reflected in the index, add to the headline reading in the same way that improving demand does. In April, delivery times extended to the maximum extent since July 2022, due to interruptions in international shipping and severe difficulties in obtaining fuel. This single factor has pushed the PMI above 50 more than any real improvement in business conditions.

The three sub-indices that more directly reflect economic activity, new orders, production and employment, all remained in contraction. Production fell for the third month in a row and at its fastest rate in 16 months. New orders continued to decline, with export business declining for the first time in four months as external demand declined. Hiring was reduced for the second month in a row as companies responded to lower workloads by reducing work hours and not replacing departing employees.

Inflation data is where the report becomes most important to the broader economic outlook. Input cost inflation accelerated to its fastest pace in more than four years in April, with nearly 69% of manufacturers surveyed reporting higher costs during the month. Fuel was the dominant driver, as a direct result of the energy price shock caused by the conflict in the Middle East. Output price inflation also rose, reaching the highest rates recorded in the decade-long history of the survey, indicating that manufacturers are passing on costs at a strong pace.

Against this backdrop, manufacturers took the unusual step of building input inventories despite lower production requirements, with purchasing activity rising and input inventories increasing for the first time in seven months. The rationale was clearly defensive: to secure materials ahead of expected further price rises and supply delays rather than any expectation of improved orders.

Business confidence fell for a third straight month to its lowest levels since July 2024. The conflict in the Middle East, the inflation it is generating and broader cost-of-living pressures have been repeatedly cited as concerns. Some optimism persists about next year, provided a resolution to the conflict is reached, but for now working conditions are worsening with each passing month.

—

The headline PMI number is misleading and markets should see it through. A reading of 51.3 driven almost entirely by supply chain delays and safety stock builds is not a sign of improving demand conditions; It’s a distress signal dressed in expansionist clothing. The three most important sub-indices of real economic activity, new orders, production, and employment, were all in contraction.

A reading of input cost inflation at a four-year high, with output price inflation among the fastest in the decade-long history of the survey, is a figure that will worry the RBA. If these price pressures persist and spread to the broader economy, the case for lowering interest rates will weaken further. The decline in business confidence for the third month in a row to its lowest levels since July 2024 underscores the fragility of the outlook.