Brazil’s Cobom unanimously cut the Selic rate by 25 basis points to 14.50% but did not provide any forward guidance, warning that future moves depend on the depth and duration of the conflict in the Middle East and that inflation expectations are further off target.

summary:

- Coboom cut the Selik interest rate by 25 basis points to 14.50% on Wednesday in a unanimous decision, which was in line with expectations of 31 of 35 economists in a Reuters poll.

- The committee did not provide any advance guidance for the second meeting in a row, saying that future price adjustments would include new information about the depth and duration of the conflict in the Middle East.

- Policymakers pointed to disjointed inflation expectations, rising headline and core inflation, and forecasts moving further above the 3% target, reinforcing a calm and cautious stance.

- The easing cycle began in March with an initial cut of 25 basis points from an almost 20-year high of 15.00%, with the central bank citing a very restrictive policy stance as justification for initiating the cuts.

- The Focus poll’s 2026 IPCA forecast rose for six straight weeks to 4.80%, above the target ceiling of 4.50%, driven by a pass on energy prices in the Iran war.

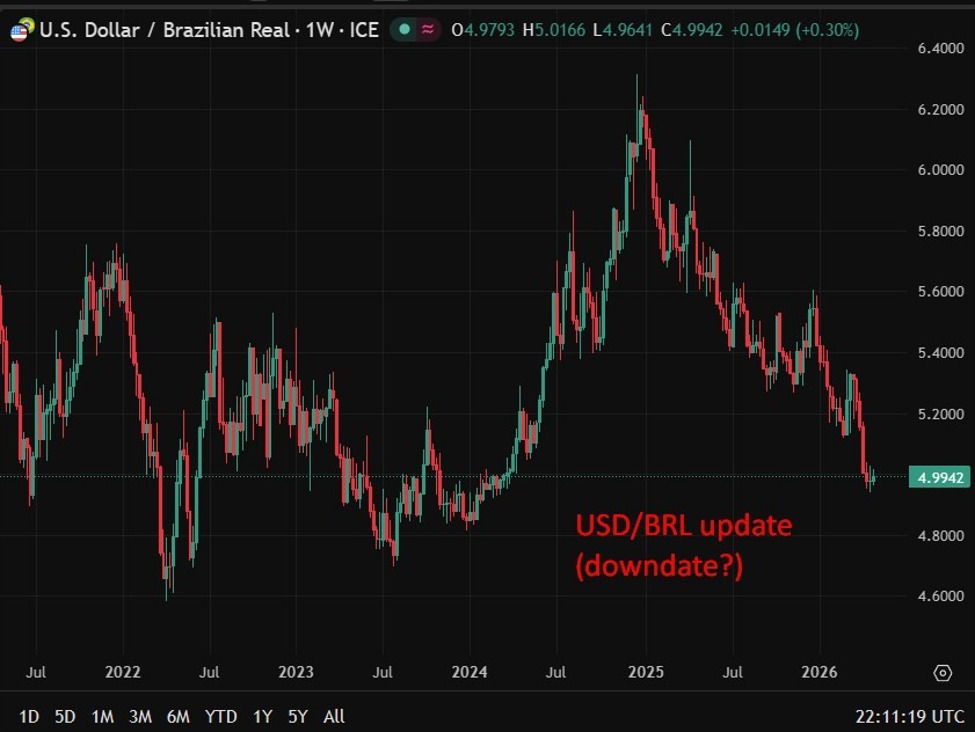

- The Brazilian real has appreciated since March, supported by Brazil’s wide interest rate differential with advanced economies, which has helped contain imported inflation pressures.

- Coboom also noted the continuous monitoring of domestic financial policy developments and their impact on financial assets and monetary conditions

Brazil’s central bank cut its benchmark Selec interest rate by 25 basis points to 14.50% on Wednesday, making its second straight cut since launching an easing cycle in March, but the accompanying statement made clear that policymakers see the path ahead as narrow, conditional and increasingly complicated by external forces.

The vote was unanimous by the interest rate setting committee, known as COBOM, and the result was in line with the expectations of the vast majority of market economists. But the language surrounding the decision was remarkably cautious. Decision makers stressed the need for calm and caution and refused to hold a second meeting in a row to provide guidance on future moves, instead conditioning the pace of additional cuts on information received about the depth and duration of the conflict in the Middle East. The Iran war and its effects on global energy prices, supply chains and broader growth prospects created a layer of uncertainty that the Committee was not prepared to consider.

The domestic inflation picture is not cooperating. Coboom explicitly stated that headline inflation and core inflation measures have risen and are moving further above the 3% target, and that uncertainty about the outlook has increased significantly. Inflation expectations remain unsteady, the labor market is adding to price pressures, and a Focus survey of market economists has revised IPCA’s 2026 forecast upward for six straight weeks, to 4.80%, above the 4.50% upper end of the target tolerance band. Before the Hormuz crisis began to reshape global energy markets, analysts expected Brazil’s inflation rate to reach less than 4% for this year.

The context of the pieces is important. The Selec has been held at 15.00%, the highest level in almost 20 years, since July 2025 as COBOM followed a strong tightening cycle to pull inflation back to target. The justification for initiating easing was the exceptionally restrictive level of interest rates rather than any tangible improvement in inflation expectations, and this framework remains unchanged. Brazil carries one of the highest real interest rates in the world, and the wide spread with advanced economies has helped support the Brazilian real since the March meeting, as the stronger currency reduces the cost of imports and provides some compensation for price pressures caused by energy.

The committee also noted the continued monitoring of domestic financial policy and its interaction with monetary conditions and financial assets, in reference to the ongoing tension between financial expansion and the central bank’s mandate to achieve price stability. Any deterioration on this front, coupled with further escalation in the Middle East, would quickly erode the already weak case for further easing, and could bring the cycle to a complete halt in the coming months.

Coboom (Comitê de Política Monetária) is Brazil’s monetary policy committee, the equivalent of the Federal Open Market Committee (FOMC) or the Monetary Policy Committee (MPC) of the Bank of England. It meets every 45 days to set interest rates and is part of the Banco Central do Brasil.

Selleck (Sistema Especial de Liquidação e Custódia) is the benchmark overnight interest rate in Brazil, which is equivalent to the federal funds rate or the base rate of the Bank of England. It is the primary tool that COBOOM uses to control inflation which is the rate at which banks lend to each other on an overnight basis using government bonds as collateral.