Another crisis for the markets.. Build your strong portfolio to bear anything

For nearly a thousand years, Theodosia’s Walls of Constantinople (modern-day Istanbul) have remained one of the strongest defenses ever built.

The strength of the Theodosian Walls did not come from a single imposing barrier, but from a carefully designed and layered system.

A wide trench stretched across the front, slowing the invaders before they could even reach the structure. Behind it was an outer wall, and behind it a longer and thicker inner wall.

The towers were spaced at regular distances along the walls, giving the defenders visibility and the ability to strike from multiple angles. Even if attackers managed to penetrate a single layer, they found themselves exposed in the open space between the walls, vulnerable before they could move forward.

Underneath it all was a solid foundation, designed to last for centuries, supported by constant maintenance and enhancement.

These walls had depth, repetition and strength beneath the surface. They are not built for looks but for endurance.

This is exactly the kind of power the market demands today.

Titles that may be missing

Operation Epic Fury has created a great deal of uncertainty in the markets. But while investors focus on the immediate headlines, a quieter risk is brewing beneath the surface – one with the potential to inflict much longer-term damage to long-term fortunes.

That’s why today’s environment needs a different kind of portfolio – one built like a fortress.

The deepening crisis in the private credit market is flying under the radar of most investors. If not for the war, these headlines would have created more anxiety.

from Bloomberg:

from CNN:

The private credit industry — worth an estimated $1.8 trillion — is struggling with massive defaults and fears that disrupting artificial intelligence will hurt software companies, which account for about 30% of its loans, according to JPMorgan.

Earlier this week, Apollo Global Management and Ares said they were limiting shareholder withdrawals from their credit funds amid an increase in investor demands across the industry.

Meanwhile, Moody’s downgraded the credit rating of a private credit fund run by KKR and Future Standard, sending it into “junk” territory after more borrowers stopped repaying their loans.

Investment myth Louis Navellier has been calling out this danger for more than a year.

In December, during our semi-annual A wish At a roundtable with all the analysts, Lewis was optimistic about the market’s prospects in 2026, but described this issue as one to watch.

If you want to be afraid, private credit is a problem.

Dodd-Frank created the private credit industry because banks wouldn’t lend to people unless they were perfect. So, if your credit score isn’t higher than 800, you’re 798, they’ll kick you out into private credit, mark up the loans, and pay 11% returns to investors because they’re profiting off those loans. Well, now the default rate is rising, there’s a problem.

JP Morgan lost $170 million with Tricolor. BlackRock has trouble with loan pool in Utah; They may lose half a billion dollars.

Since then, the negative headlines have come quickly.

Now, you might be thinking…

“Why should I care about private credit? I don’t have any of that money.”

Even if you’ve never invested a dollar in private credit… Many companies own it Depend on it.

As Lewis said, this has quietly become a $1.8 trillion market The ideal financing source for thousands of businesses that were unable to qualify for traditional bank loans. This is especially true in areas such as software, where easy money has helped fuel rapid growth.

For many years, this system has kept weaker companies alive, helped others expand more quickly than fundamentals justified, and allowed investors to ignore weaknesses.

But that environment has changed.

Interest rates are higher. Defaults are on the rise. Lenders began to back away.

Many companies taking advantage of this cheap money are about to lose access to the very thing that keeps them afloat. When this happens, the effect will not remain confined to private credit funds – the ripples will ripple throughout the stock market.

You can probably guess what we’ll see.

Companies miss profits. It becomes difficult to refinance debt. Layoffs begin.

Then stock prices fall rapidly.

Therefore, you don’t have to be in the private credit market to start feeling the effects.

You just have to own the wrong stocks.

Can your wallet handle the stress?

Just as Theodosian Walls were not defined by a single layer of stone… the most powerful companies today are not defined by a single measure.

They are built in layers.

This is exactly what the Louis Navellier system was designed to recognize.

Each week, Lewis performs a quantitative analysis of more than 6,000 stocks, rating them from A to F based on the same kind of structural strength that made those walls so effective.

It is not superficial features such as noise or recent price momentum, but the deeper layers that determine this Whether the company can handle real pressure.

We’re talking about stocks with superior fundamentals:

- Strong and consistent cash flow

- High return on equity

- Expanding profit margins

- Low debt compared to assets

Of course, whether institutional investors are quietly accumulating shares.

When all of these layers are in place, stocks get an “A” in Louis’ Stock Grader system.

These are the real fortified companies in the market.

On the other hand, it is stocks with weak fundamentals, such as high debt, deteriorating margins, and negative cash flow, that rely on today’s private credit system to survive.

If this system continues to crack, there will be no second wall behind it.

Citadel DNA

In Lewis Stock breakout Service, he recommends small companies with superior fundamentals…those that few have heard of that can soar higher over time.

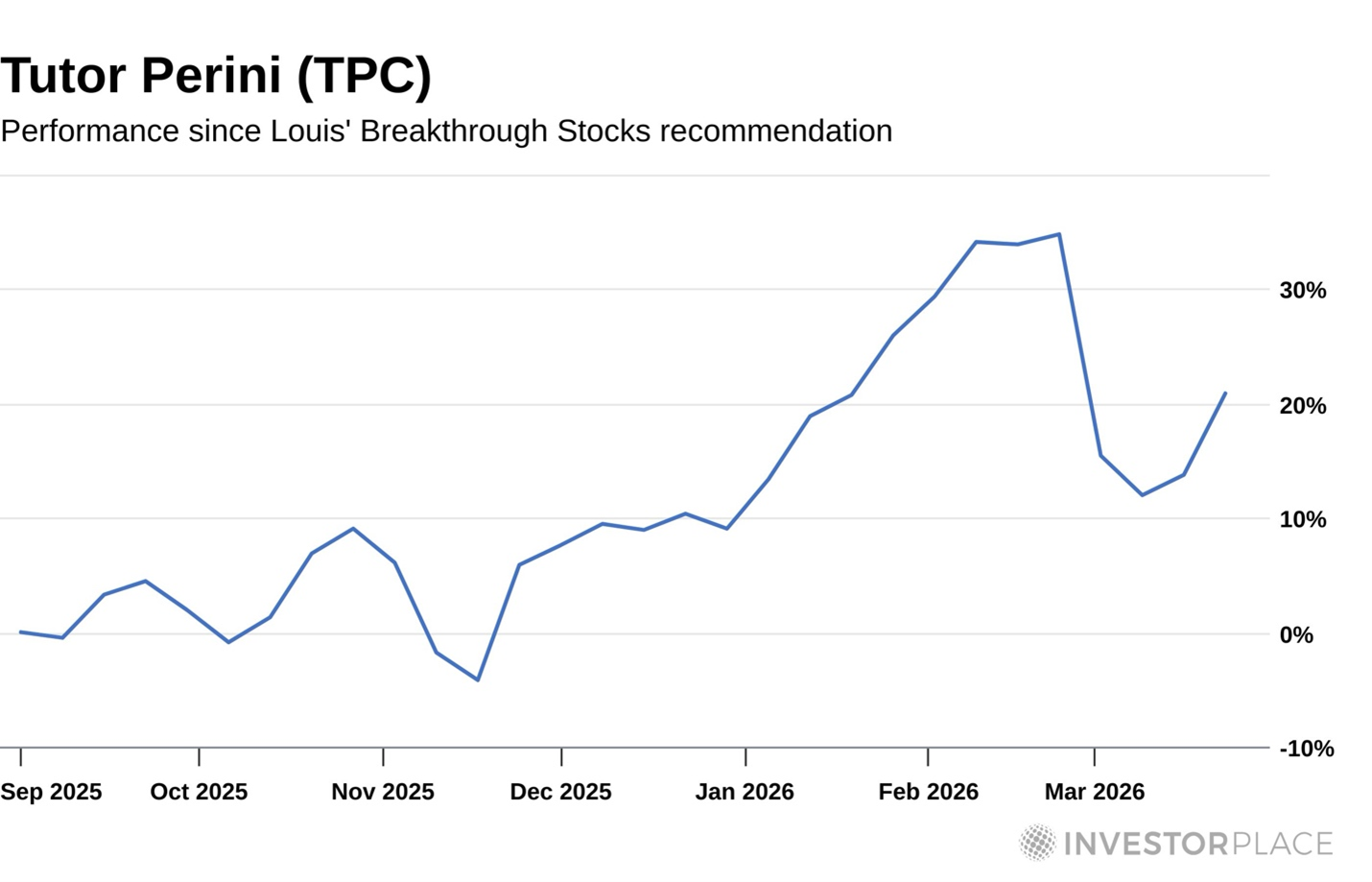

In September, he recommended Tutor Perini Corp. (TPC), a full-service contracting company.

This is not my flashy AI darling. Instead, it is a company widely known for large-scale transportation and civil construction. In late February, the company reported huge earnings, proving why the Lewis System identifies it as a strong buy.

Adjusted earnings for the fourth quarter rose to $1.07 per share, compared to a loss of $1.49 per share in the same quarter a year earlier. The consensus estimate called for adjusted earnings of $0.92 per share, so TPC posted Earnings surprise 16.3%. Fourth-quarter revenue rose 41.1% year over year to $1.51 billionExceeding estimates of $1.35 billion.

Even with the recent market volatility, the stock has held up well and is rising more than 20%.

The stock is below Lewis’ buy price of $90, so there is still time to enter this trade.

Lewis just released a deep dive into the growing cracks in private credit that doesn’t just include details How to protect your wallet, but how to benefit This crisis is redirecting massive flows of capital through the financial system.

As I noted above, he identified this risk months ago, and has been putting his subscribers in the best position to protect themselves — and even profit — when the market starts to show cracks.

Maybe you’re a member of a trust, or maybe you’re exposed to collateral damage without realizing it – either way, you need to make the time Watch Luis’ free presentation that explains the risks and can help you make a profit.

Enjoy your weekend,

Luis Hernandez

Editor-in-Chief, InvestorPlace